Duration: 1 month, 2024

Area of Focus: UX, Interaction

Team: Arundhuti Dey

PROJECT OVERVIEW

Who hasn't felt that sinking feeling when checking their bank account and wondering, "Where did all my money go?". The modern financial landscape, with its myriad transactions and payment methods, can make tracking expenses a real headache. It's like trying to find a needle in a haystack, but with less satisfaction and more stress.

This project aims to identify gaps in the tracking system available today in the market and improve the quality of such services.

01. Background & Problem Area

02. Research & Analysis

03. Ideation

04. Final Construction & Testing

Process Overview

Project Overview

01

Background & Problem Area

Keeping track of expenses is an essential task which helps with one’s financial well-being. Understanding spending patterns, building emergency funds, savings and achieving financial goals are key benefits.

While digital tools make tracking expenses easier, many still struggle. "Remember the days of meticulously balancing checkbooks and filing receipts? In today's digital age, tracking finances should be a breeze. Yet, many of us still struggle to stay on top of our expenses. Why is it so difficult to keep our financial house in order, even with all the technology at our fingertips?"

The many factors affecting this problem may inculde:

Behavioural/ Habits

Integration Challenges

Overwhelming Choices

Privacy Concerns

Complexity of Modern Finances

Cost and Time

“Do not save what is left after spending but spend what is left after saving.”

— Warren Buffet

01

Background & Problem Area

Keeping track of expenses is an essential task which helps with one’s financial well-being. Understanding spending patterns, building emergency funds, savings and achieving financial goals are key benefits.

While digital tools make tracking expenses easier, many still struggle. "Remember the days of meticulously balancing checkbooks and filing receipts? In today's digital age, tracking finances should be a breeze. Yet, many of us still struggle to stay on top of our expenses. Why is it so difficult to keep our financial house in order, even with all the technology at our fingertips?"

The many factors affecting this problem may inculde:

Behavioural/ Habits

Integration Challenges

Overwhelming Choices

Privacy Concerns

Complexity of Modern Finances

Cost and Time

“Do not save what is left after spending but spend what is left after saving.”

— Warren Buffet

02

Research & Analysis

Literature Review

An extensive literature review was conducted to assess the current understanding of spending and tracking pattens of individuals. It involved reading about financial capabilities of people, implications of the digital era on personal finances and money-management behaviours.

Why is it important to keep track of one’s personal expenditure and budget?

Financial management positively influences financial well-being.

One of the five domains related to good financial capabilities is expense management along with managing money in terms of making ends meet, planning ahead, choosing financial products and staying informed.

Aids with self-control over spending

How has the popular adoption of cashless payments impacted spending and

saving habits in India?

Using digital payment tools...

As per the report published by ACI Worldwide in 2022, India leads globally in terms of real–time payment transactions with 48.6 billion transactions processed in 2021.

Spending habits have changed in nearly the last decade as the world transforms into a cashless one. It is due to increased convenience and accessibility, reduced friction in payments and contributed to the rise of digital commerce.

In a remarkable surge reflecting the growing popularity of digital payments, Unified Payments Interface (UPI) transactions in India soared by 52% year-on-year, reaching 78.97 billion in the first half of 2024.

Interestingly, the average ticket size (ATS) of UPI transactions saw a decline from INR 1,603 in the first half of 2023 to INR 1,478 in 2024. This 8% drop, particularly in person-to-merchant transactions, indicates that UPI is becoming increasingly popular for small, everyday purchases.

Digital transactions help the transactions to occur in real-time hence minimizing the consumer's inability to resist the temptation to buy products they do not need.

People feel more in control of their tracking of spending habits.

UPI payment apps provide a transaction history

the transaction history provides no categorisation

“Pain of the tangible is non-existant”

According to Prelec & Loewenstein in 1998, binary form of money reduces pain of spending, thus triggering future spending. (Kaakandikar et. al. 2024)

possibility of impulse buy increases

studies have shown that the

convenience that is offered by digital wallets suggests that the users are prone to overspending because the activity that is being conducted is less tangible and more convenient (Thomas et al ., 2020).

02

Research & Analysis

Literature Review

An extensive literature review was conducted to assess the current understanding of spending and tracking pattens of individuals. It involved reading about financial capabilities of people, implications of the digital era on personal finances and money-management behaviours.

Why is it important to keep track of one’s personal expenditure and budget?

Financial management positively influences financial well-being.

UPI payment apps provide a transaction history

the transaction history provides no categorisation

People feel more in control of their tracking of spending habits.

Digital transactions help the transactions to occur in real-time hence minimizing the consumer's inability to resist the temptation to buy products they do not need.

Aids with self-control over spending

One of the five domains related to good financial capabilities is expense management along with managing money in terms of making ends meet, planning ahead, choosing financial products and staying informed.

How has the popular adoption of cashless payments impacted spending and saving habits in India?

Using digital payment tools...

possibility of impulse buy increases

studies have shown that the

convenience that is offered by digital wallets suggests that the users are prone to overspending because the activity that is being conducted is less tangible and more convenient (Thomas et al ., 2020).

“Pain of the tangible is non-existant”

According to Prelec & Loewenstein in 1998, binary form of money reduces pain of spending, thus triggering future spending. (Kaakandikar et. al. 2024)

As per the report published by ACI Worldwide in 2022, India leads globally in terms of real–time payment transactions with 48.6 billion transactions processed in 2021.

Spending habits have changed in nearly the last decade as the world transforms into a cashless one. It is due to increased convenience and accessibility, reduced friction in payments and contributed to the rise of digital commerce.

In a remarkable surge reflecting the growing popularity of digital payments, Unified Payments Interface (UPI) transactions in India soared by 52% year-on-year, reaching 78.97 billion in the first half of 2024.

Interestingly, the average ticket size (ATS) of UPI transactions saw a decline from INR 1,603 in the first half of 2023 to INR 1,478 in 2024. This 8% drop, particularly in person-to-merchant transactions, indicates that UPI is becoming increasingly popular for small, everyday purchases.

Survey

To understand the existing nature of payments done by users and their methods/tools of keeping a check on their expenditure and balance, a survey was conducted. As we move towards a more and more digitized world, more focus was put on young adults as their thoughts and opinions matter when it comes to shaping the expense tracking services, given that they are the largest upcoming stakeholder of these services

How efficient are the current ways of tracking?

monthly budgeting

63.2%

31.6%

5.3%

5.3%

6834

others

predicting lifestyle patterns

impulse buying

savings

What does tracking expenses help you with?

use UPI as their main method of payment

implies that they have a record of most of their payments on the app itself.

75%

of the respondents who don’t track their expenses(43.8%) currently for various reasons are willing to do so if they find the right tool

85.7%

of the respondents would like to track their expenses daily and 16.7% of them would like to track them at least twice a week.

75%

of the respondents would like to track their expenses daily and 16.7% of them would like to track them at least twice a week.

75%

of all the respondents track their expenses on a regular basis

52.2%

Frequency of tracking expenditure and its benefits

of the respondents are not very keen on entering each transactions they perform

94.8%

Given that all the current tracking apps that exist mostly rely on manual entries,

Only

of the respondents who track their expenditure are confident that their method of tracking is effective.

42.1%

Would you like to have an online repository of all your bills and expenses in one place?

Maybe

30.4%

4.3%

65.2%

Yes

No

Survey

To understand the existing nature of payments done by users and their methods/tools of keeping a check on their expenditure and balance, a survey was conducted. As we move towards a more and more digitized world, more focus was put on young adults as their thoughts and opinions matter when it comes to shaping the expense tracking services, given that they are the largest upcoming stakeholder of these services

85.7%

of the respondents who don’t track their expenses(43.8%) currently for various reasons are willing to do so if they find the right tool

use UPI as their main method of payment

implies that they have a record of most of their payments on the app itself.

75%

Frequency of tracking expenditure and its benefits

of all the respondents track their expenses on a regular basis

52.2%

monthly budgeting

63.2%

31.6%

5.3%

5.3%

68.3%

others

predicting lifestyle patterns

impulse buying

savings

What does tracking expenses help you with?

of the respondents would like to track their expenses daily and 16.7% of them would like to track them at least twice a week.

75%

How efficient are the current ways of tracking?

of the respondents are not very keen on entering each transactions they perform

Given that all the current tracking apps that exist mostly rely on manual entries,

94.8%

Would you like to have an online repository of all your bills and expenses in one place?

Maybe

30.4%

4.3%

65.2%

Yes

No

Only

of the respondents who track their expenditure are confident that their method of tracking is effective.

42.1%

Develop a user-centric solution to enable easy tracking of daily expenses through integration into existing solutions with automation, focusing on convenience of accessing data and gaining fruitful insights centered around financial independence and balancing of money by young adults.

Redefined Brief

Redefined Brief

Develop a user-centric solution to enable easy tracking of daily expenses through integration into existing solutions with automation, focusing on convenience of accessing data and gaining fruitful insights centered around financial independence and balancing of money by young adults.

Expense Tracking Frequency: Daily

Apps Used: Money Manager App. UPI Apps

Modes of Payment:

UPI - mostly

cash - sometimes

credit/debit card - rarely

Motivations:

go on trips with friends

not overspend on food

finds it hard to remember to track everyday expenses

too many apps to keep track of

splitting bills & tracking them is a hassle

Needs:

consolidated data on her spending

better categorisation tool

better financial management skills

Frustrations:

Priya, 23 F

Occupation: Designer

City: Bangalore

outgoing

impatient

extrovert

food lover

“ I need to track my expenses or I lose track of how much I’ve spent.”

Priya is a studio worker with 1 year of work experience. She is a free spirit who likes to travel but on budget. Being a designer, she loves to experiments with new things.

User Persona

Checking transaction histories repeatedly can be quite a hassle. So, having an automatically generated list of payments, with a clear categorization would help, I think”

“Maybe something linked with my upi/sms“

“I’d like my UPI app to allow me to restrict spending in certain categories, such as food. I want the app to generate a pie chart showing the average payments I make in different categories over a specific period.”

“Without UPI, I might not have been spending as much on food online on apps like Zomato, Swiggy. Sometimes, I regret purchases because you only needs a phone with Wifi/mobile data"

I would like the app to tell me how much I can spend a day with the current balance...or how much extra I can spend a day but still have enough until the next pay.”

“Airdrop for a bill split“

“

”

INTERVIEW GOALS:

To understand the shortcomings of existing tracking methods

To identify where the user feels frustrated. Understand the pain points.

Understanding user expectations w.r.t a tracking app

Understanding the level of importance users place on tracking expenses

Interviews

Interviews of individuals were conducted so far to understand their perception and approach towards expense tracking in depth. Here’s what people had to say

Interviews

Interviews of individuals were conducted so far to understand their perception and approach towards expense tracking in depth. Here’s what people had to say

INTERVIEW GOALS:

To understand the shortcomings of existing tracking methods

To identify where the user feels frustrated. Understand the pain points.

Understanding user expectations w.r.t a tracking app

Understanding the level of importance users place on tracking expenses

I would like the app to tell me how much I can spend a day with the current balance...or how much extra I can spend a day but still have enough until the next pay.”

“Airdrop for a bill split“

“Without UPI, I might not have been spending as much on food online on apps like Zomato, Swiggy. Sometimes, I regret purchases because you only needs a phone with Wifi/mobile data"

“I’d like my UPI app to allow me to restrict spending in certain categories, such as food. I want the app to generate a pie chart showing the average payments I make in different categories over a specific period.”

Checking transaction histories repeatedly can be quite a hassle. So, having an automatically generated list of payments, with a clear categorization would help, I think”

Priya is a studio worker with 1 year of work experience. She is a free spirit who likes to travel but on budget. Being a designer, she loves to experiments with new things.

User Persona

Priya, 23 F

Occupation: Designer

City: Bangalore

outgoing

food lover

impatient

extrovert

Modes of Payment:

UPI - mostly

cash - sometimes

credit/debit card - rarely

Expense Tracking Frequency: Daily

Apps Used: Money Manager App. UPI Apps

Motivations:

go on trips with friends

not overspend on food

Frustrations:

finds it hard to remember to track everyday expenses

too many apps to keep track of

splitting bills & tracking them is a hassle

Needs:

consolidated data on her spending

better categorisation tool

better financial management skills

“ I need to track my expenses or I lose track of how much I’ve spent.”

“Maybe something linked with my upi/sms“

”

“

User Journey Analysis

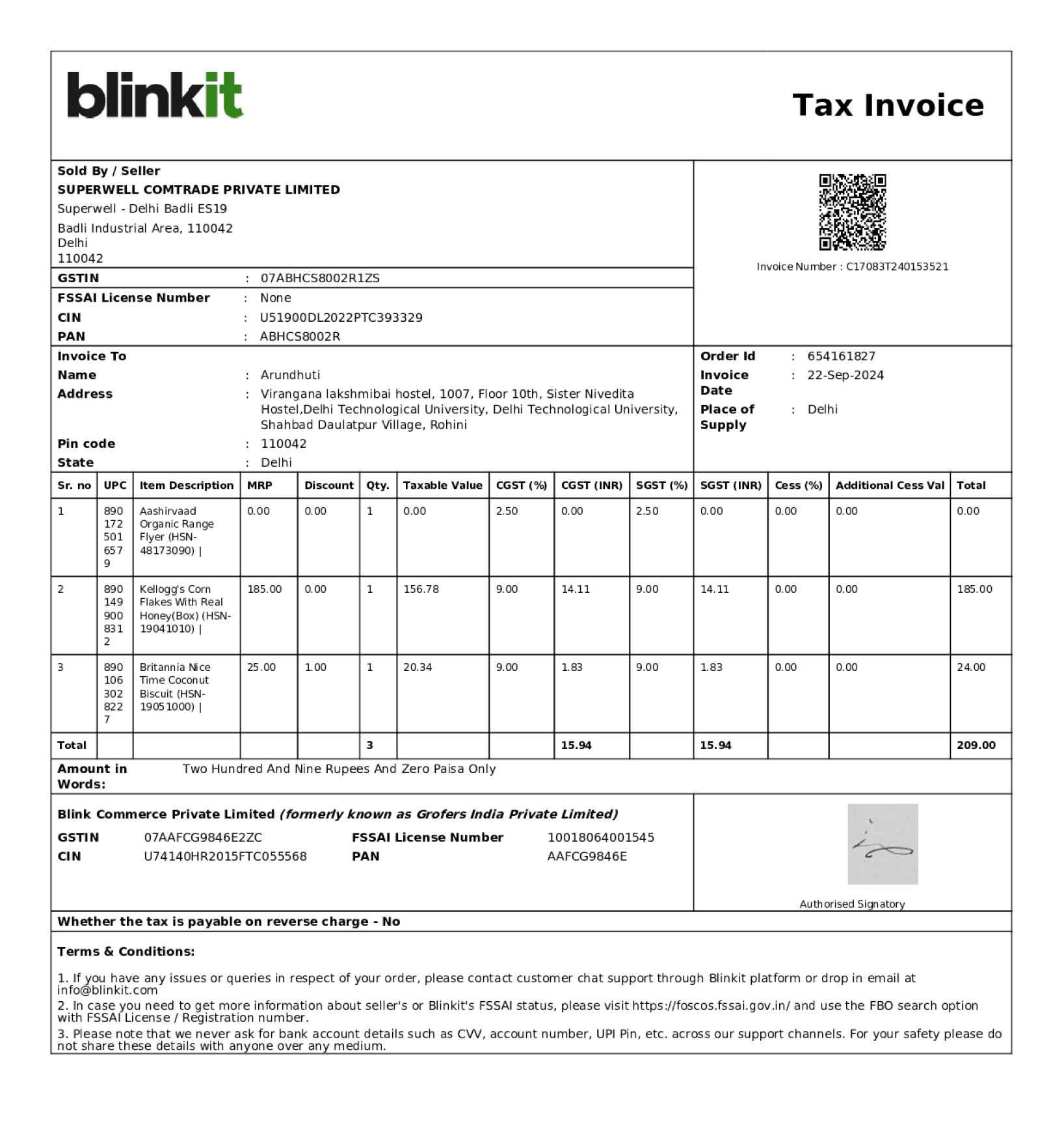

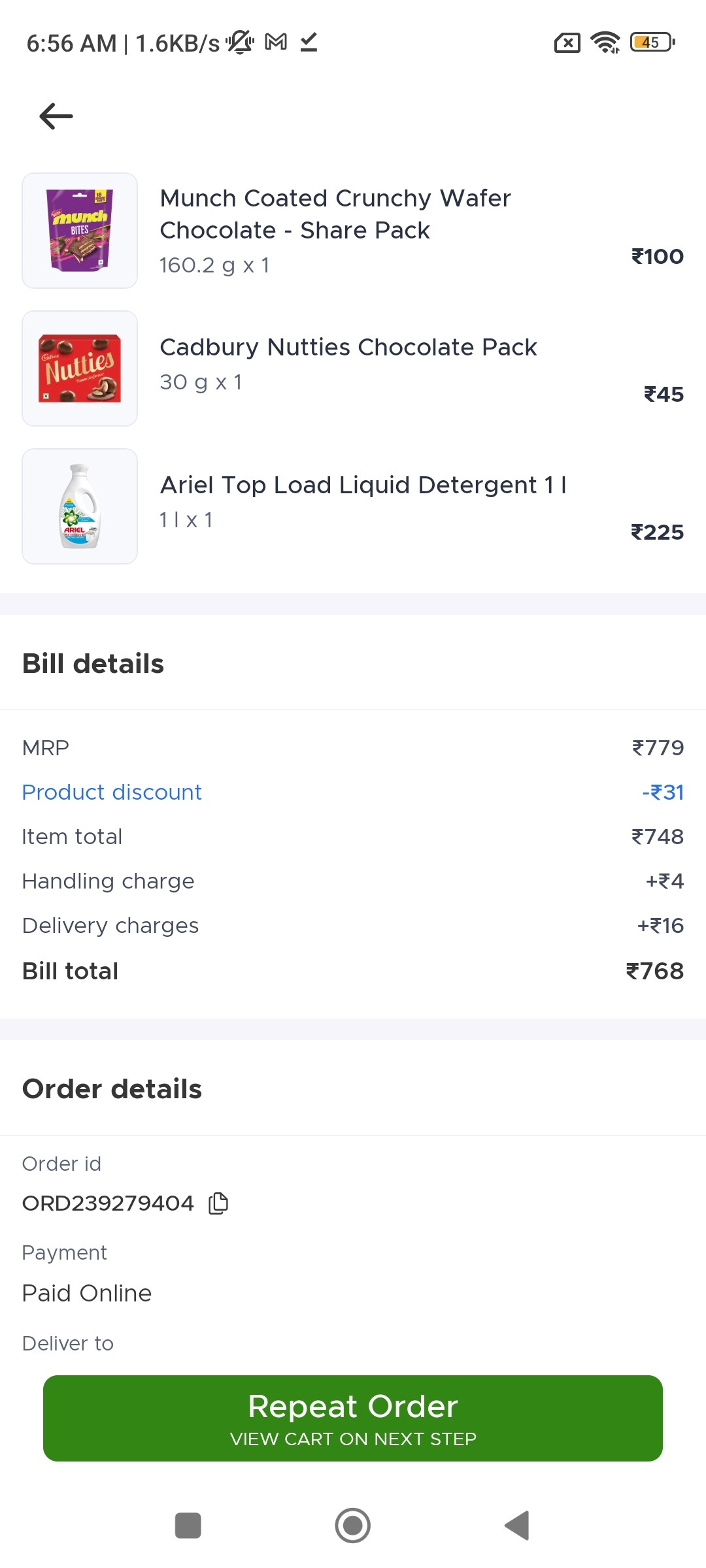

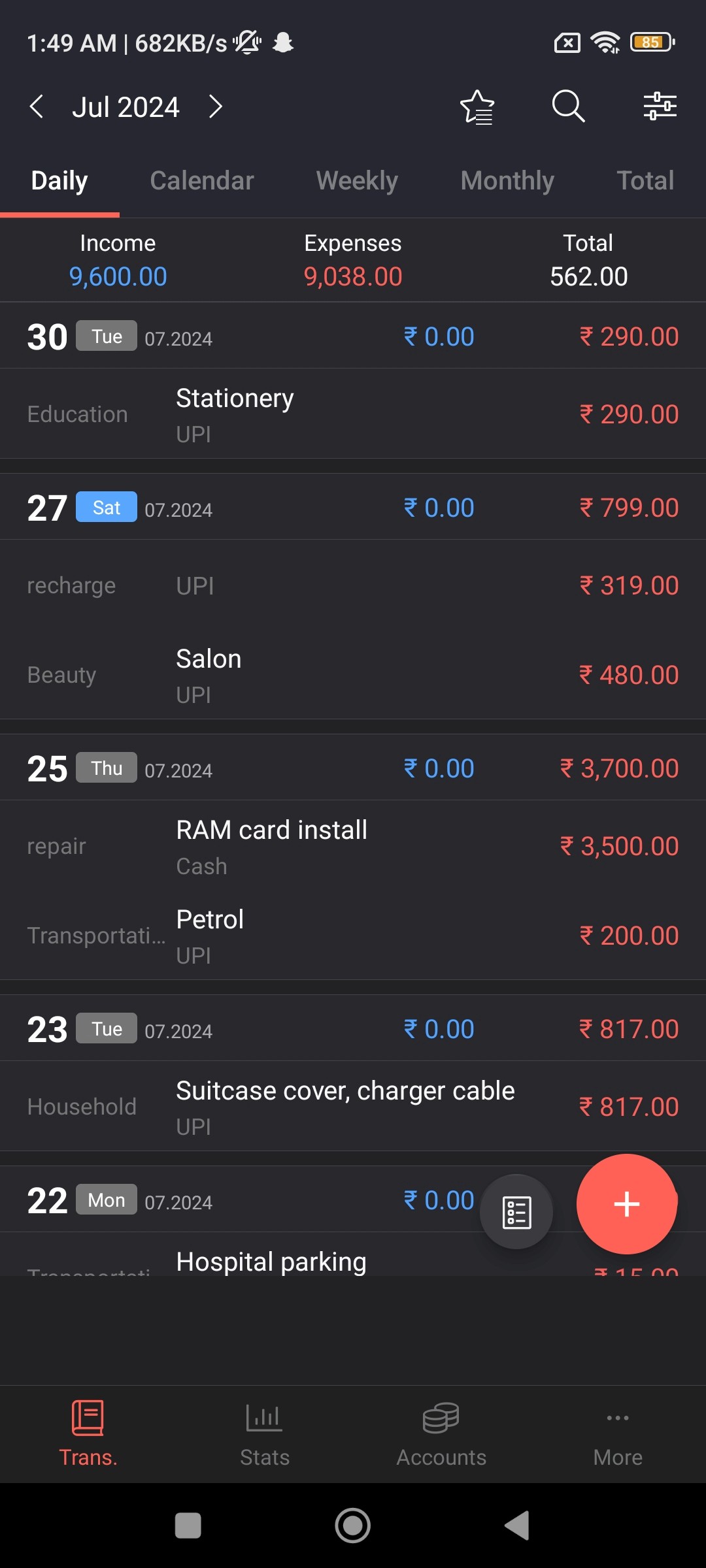

Buying groceries online from Blinkit

Select items

Add to cart

Purchase with UPI

Receive quick delivery in 10 mins

Task 1:

maintains entry for tracking expenses

refers to the online bill on the Blinkit app

uses a tracking app to manually enter the transaction details

has to categorize all items in the list to make sense of budget

SCOPE: linking online bills to tracking app

User Journey Analysis

Buying groceries online from Blinkit

Task:

Select items

Add to cart

Purchase with UPI

Receive quick delivery in 10 mins

maintains entry for tracking expenses

refers to the online bill on the Blinkit app

uses a tracking app to manually enter the transaction details

has to categorize all items in the list to make sense of budget

SCOPE: linking online bills to tracking app

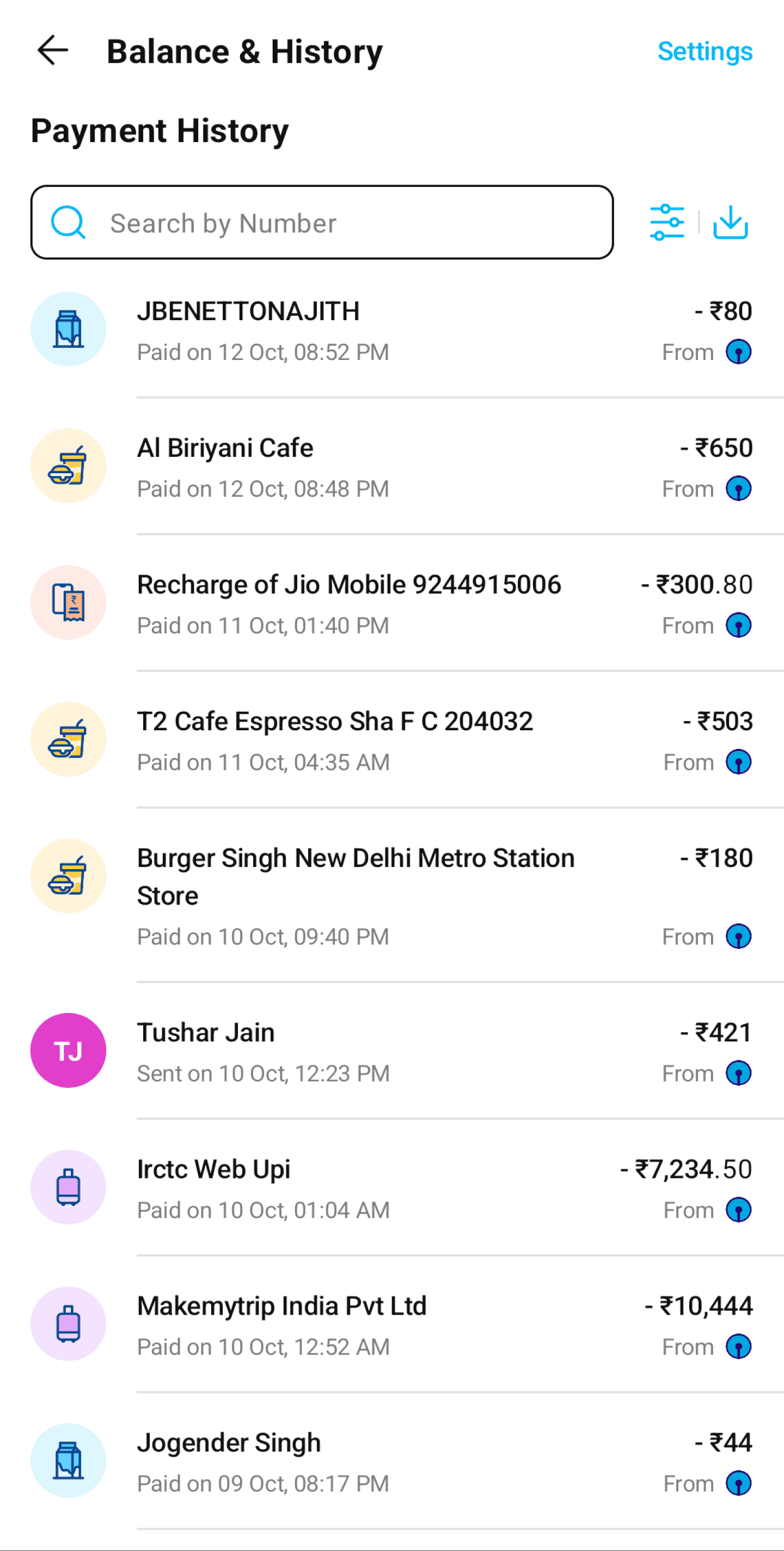

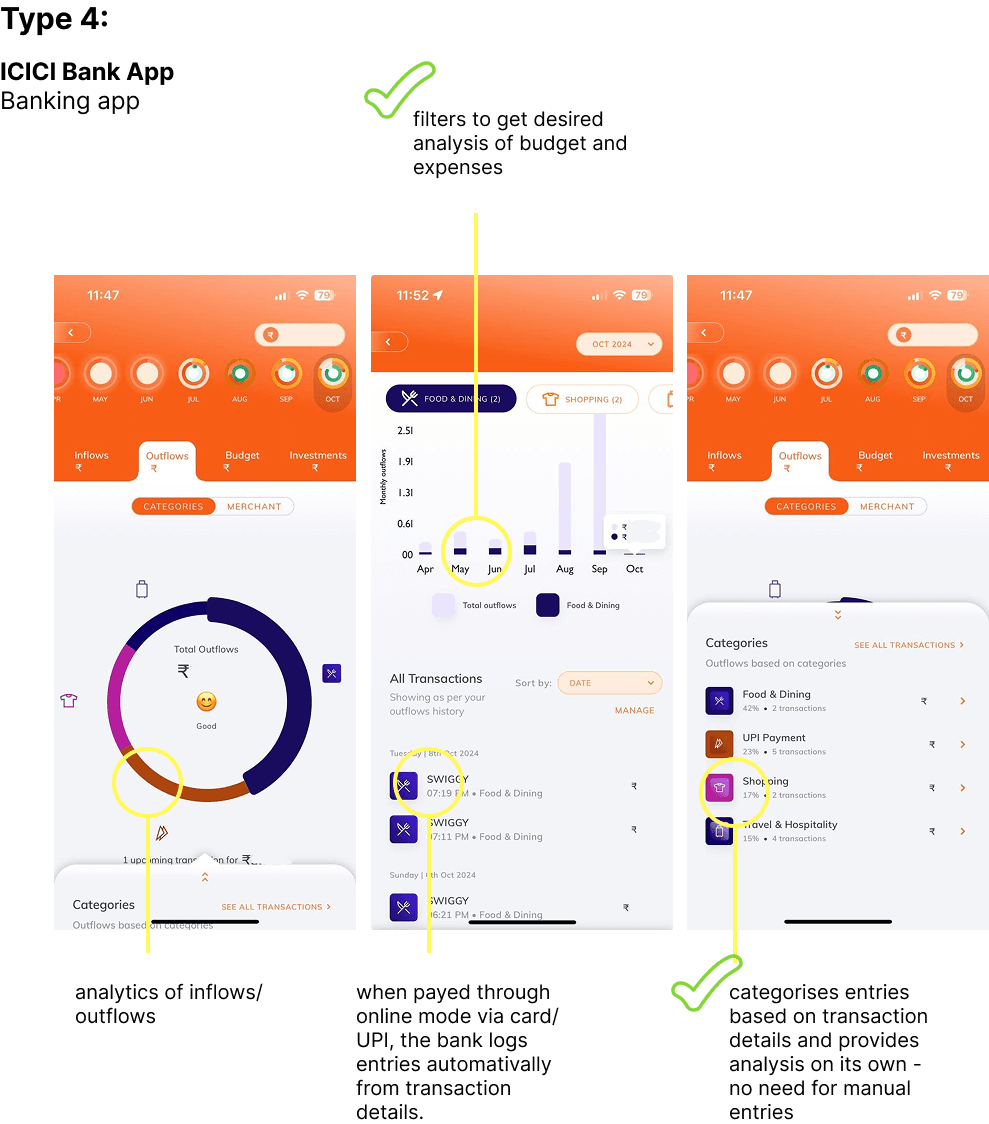

ICICI Bank App

Banking app

Type 4:

when payed through online mode via card/UPI, the bank logs entries automativally from transaction details.

categorises entries based on transaction details and provides analysis on its own - no need for manual entries

analytics of inflows/outflows

filters to get desired analysis of budget and expenses

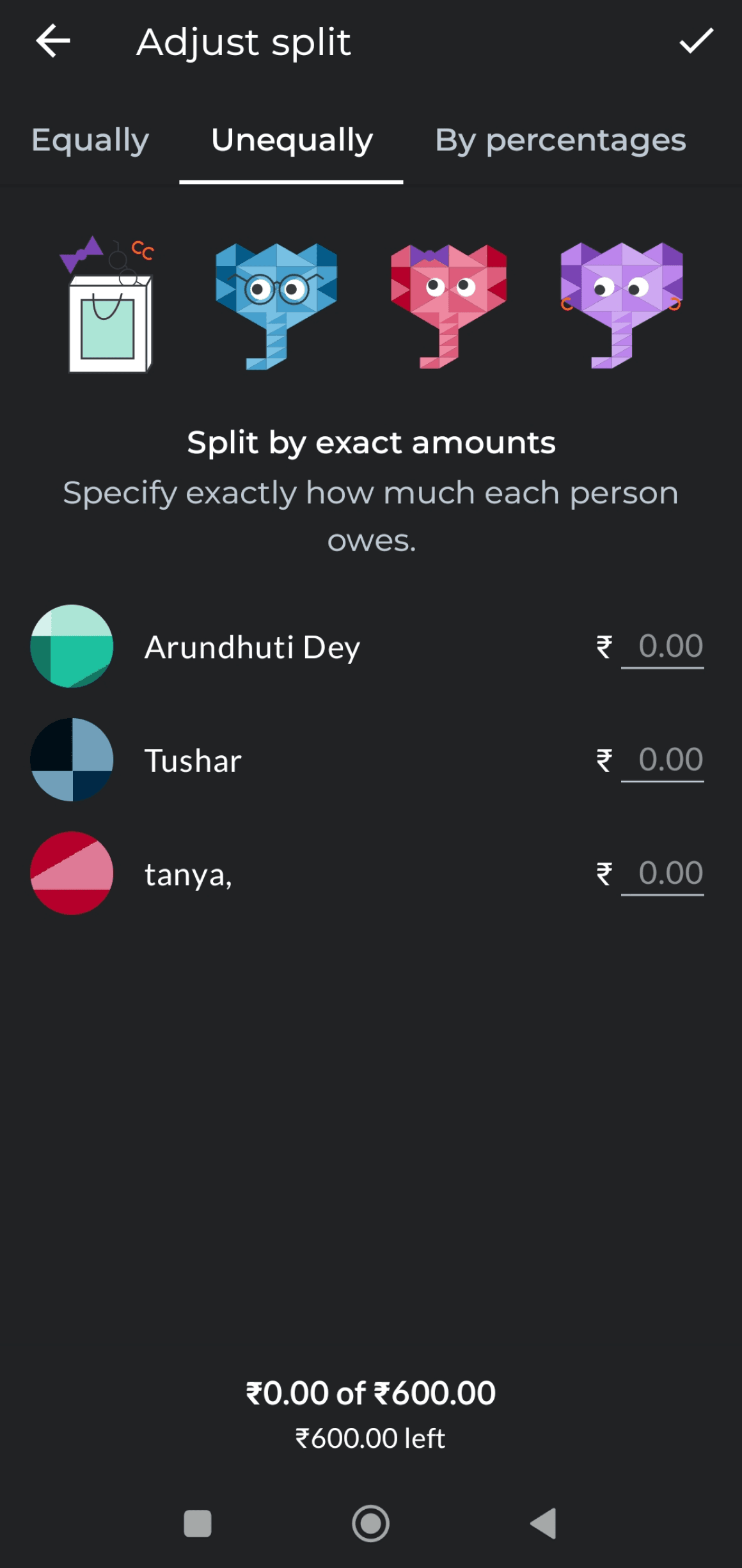

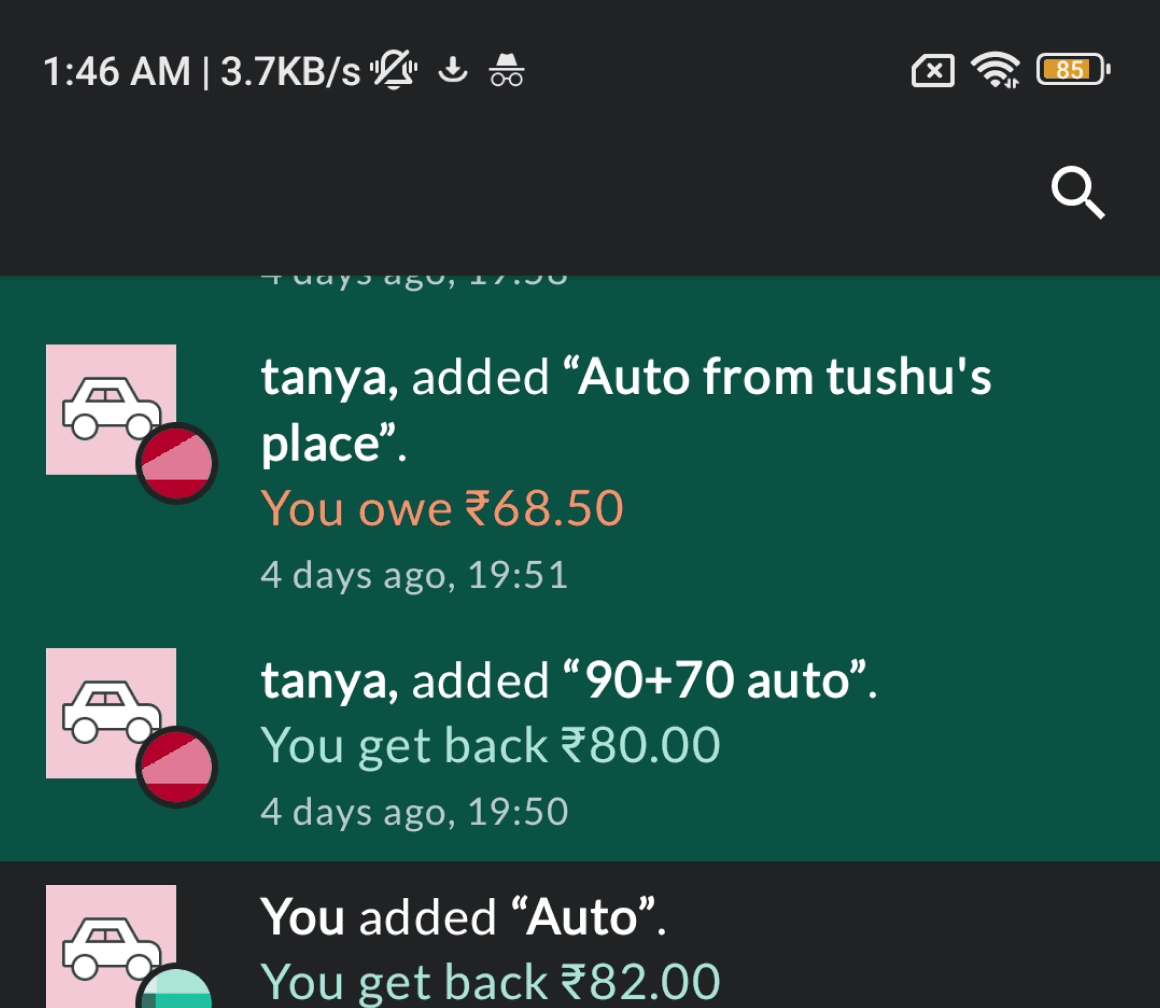

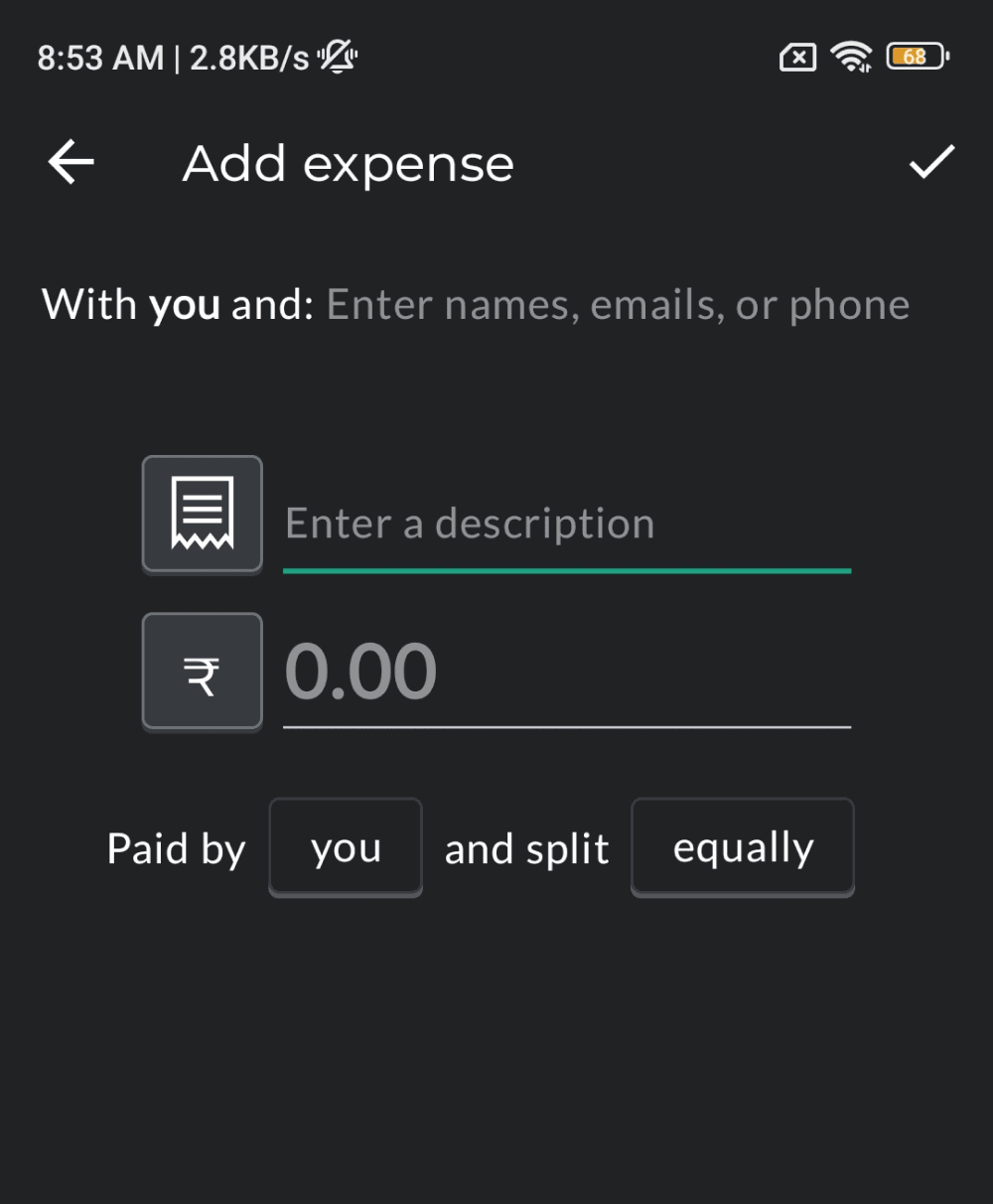

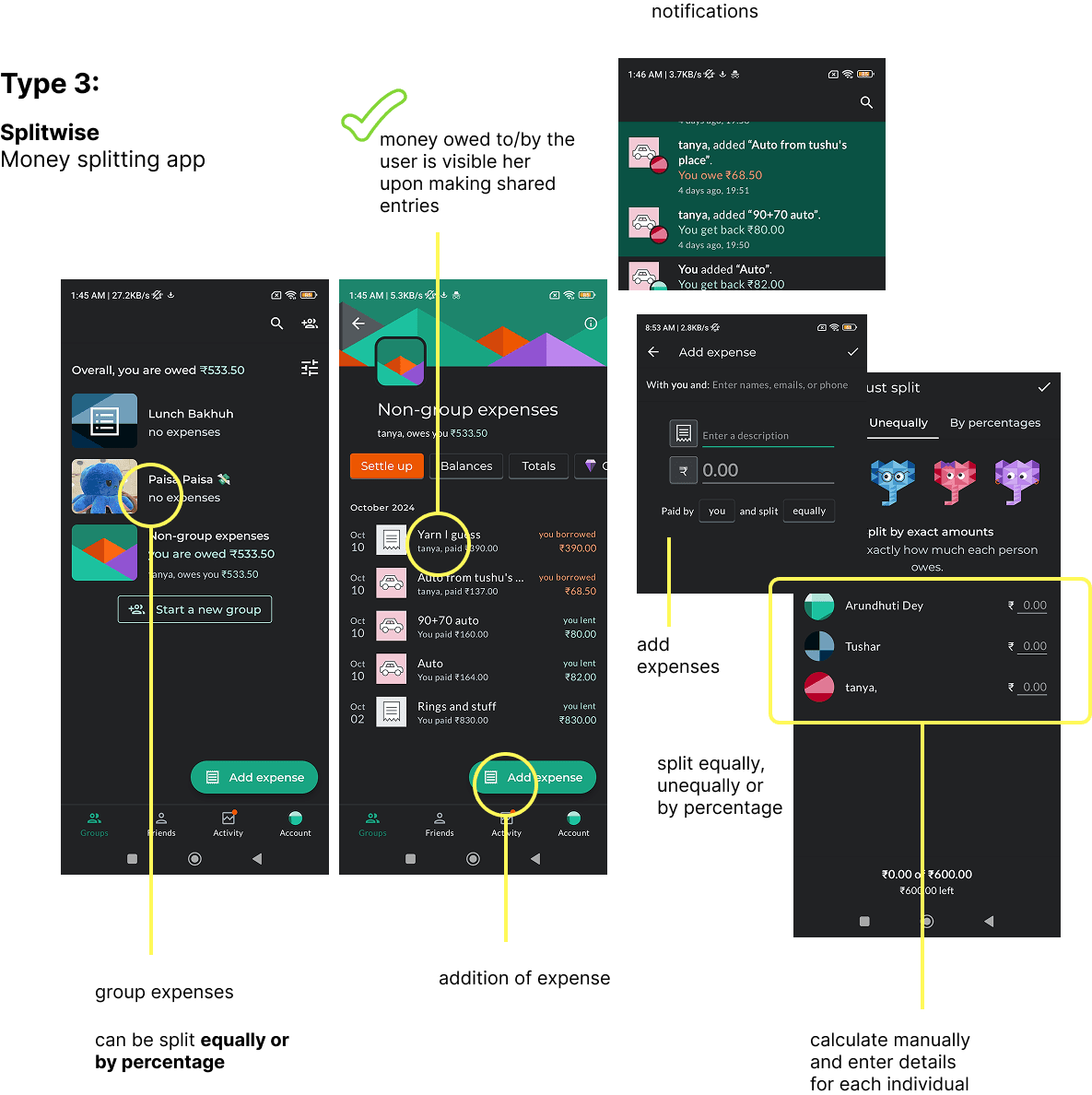

Splitwise

Money splitting app

Type 3:

addition of expense

add expenses

split equally, unequally or by percentage

calculate manually and enter details for each individual

group expenses

can be split equally or by percentage

money owed to/by the user is visible her upon making shared entries

notifications

payment history can be viewed

pre defined categories

to whom it was paid

filters to categorise transactions

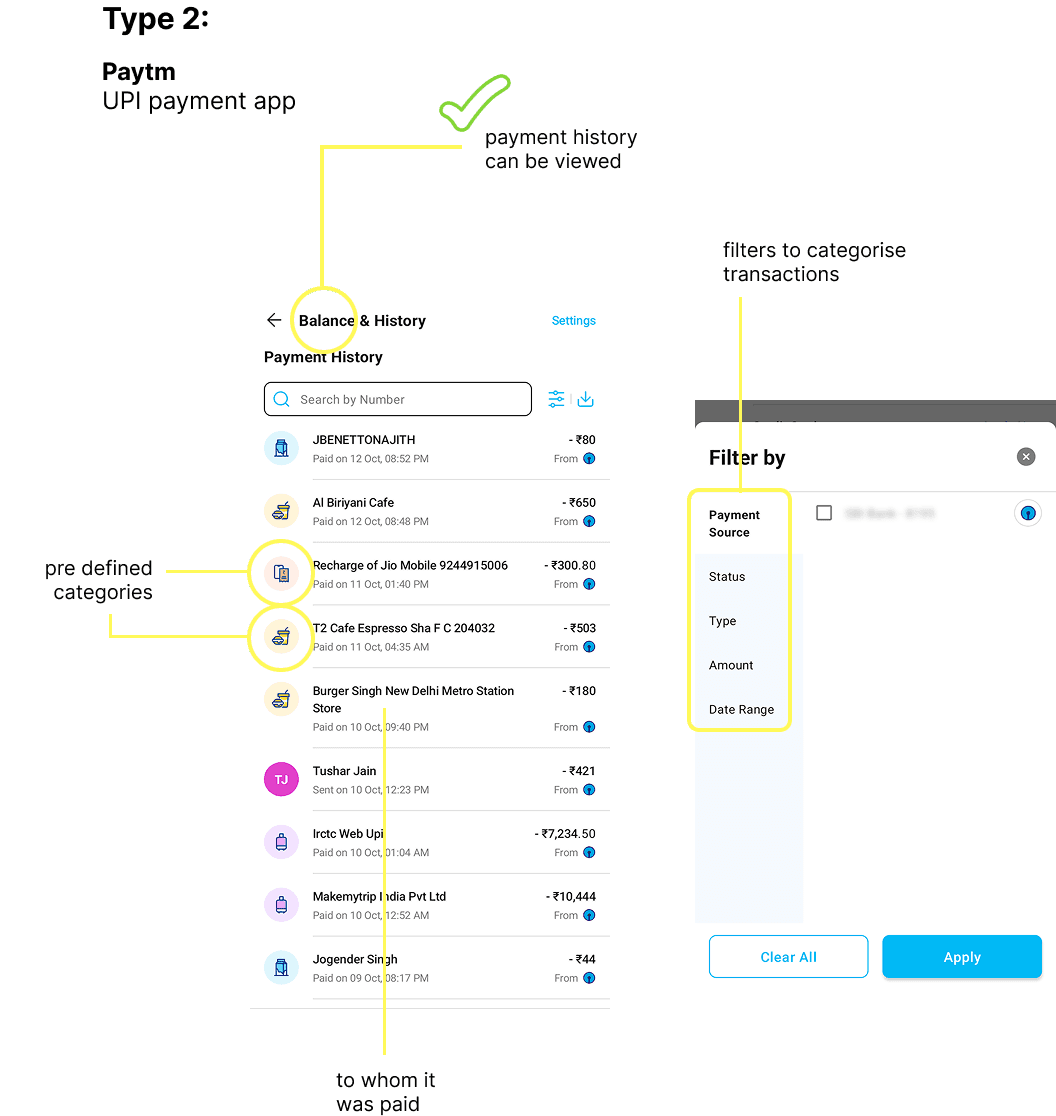

Paytm

UPI payment app

Type 2:

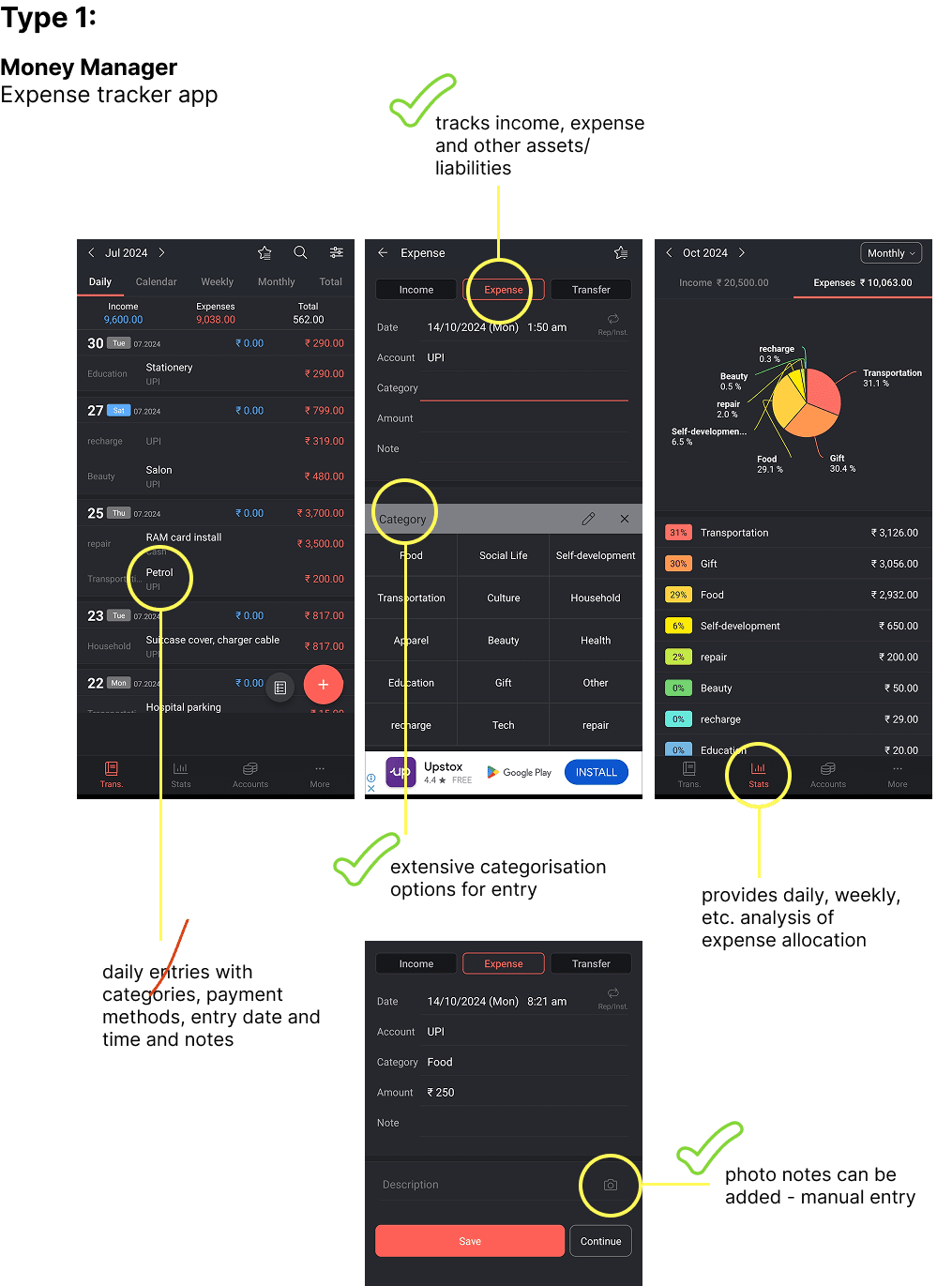

Money Manager

Expense tracker app

provides daily, weekly, etc. analysis of expense allocation

tracks income, expense and other assets/liabilities

extensive categorisation options for entry

photo notes can be added - manual entry

daily entries with categories, payment methods, entry date and time and notes

Type 1:

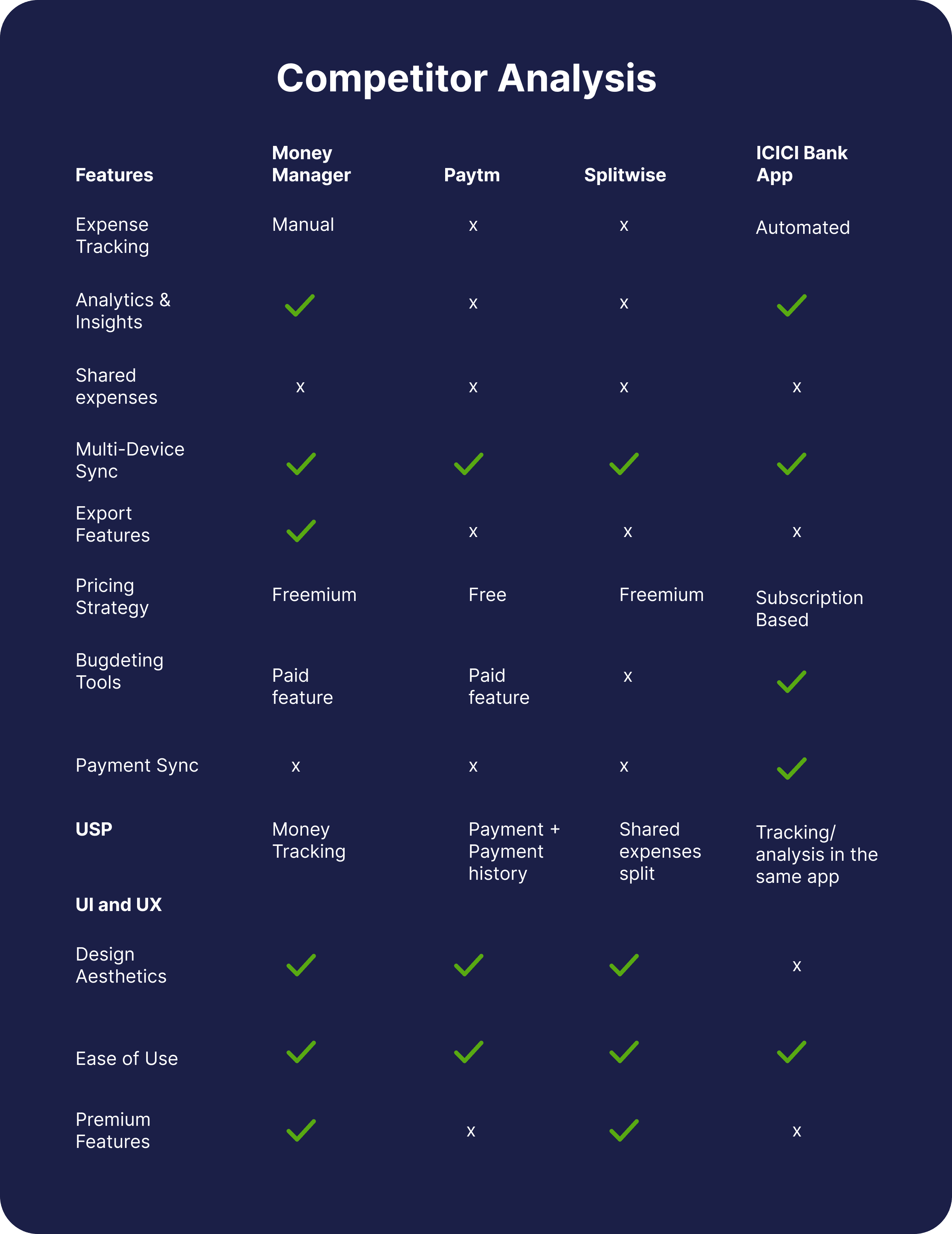

To understand the current tools available in the market, I identified competitors in the market and looked into their features. This helped in understanding what features are desirable and what they are lacking in.

To understand the current tools available in the market, I identified competitors in the market and looked into their features. This helped in understanding what features are desirable and what they are lacking in.

Current Market

Current Market

x

Shared expenses

x

x

x

x

Multi-Device Sync

Export Features

x

x

x

Subscription Based

Freemium

Freemium

Free

Pricing Strategy

x

Paid feature

Paid feature

Bugdeting Tools

Payment Sync

x

x

x

Tracking/ analysis in the same app

Shared expenses split

Money Tracking

Payment + Payment history

USP

UI and UX

Design Aesthetics

x

Ease of Use

Premium Features

x

x

Competitor Analysis

Features

Money Manager

Paytm

Splitwise

ICICI Bank App

Expense Tracking

Manual

Automated

x

x

x

Analytics & Insights

User unable to track daily expenses

forgets to make entries after every transaction

is the user unable to

WHY?

user cannot find a consistent way to track every payment with different methods of transaction

does the user forget

WHY?

Different payments methods have separate and scattered logs with cash payments being lost

Because the attention and energy is divided between multiple apps and tools with each of them having limited services

WHY?

can’t the user find a consistent way to track

WHY?

are different logs difficult to track for the user

Root Cause Analysis

Root Cause Analysis

User unable to track daily expenses

is the user unable to

WHY?

forgets to make entries after every transaction

WHY?

does the user forget

user cannot find a consistent way to track every payment with different methods of transaction

WHY?

can’t the user find a consistent way to track

Different payments methods have separate and scattered logs with cash payments being lost

WHY?

are different logs difficult to track for the user

Because the attention and energy is divided between multiple apps and tools with each of them having limited services

Current Situation

Current Situation

Survey insights revealed that young individuals track expenses for specific financial goals, like saving for a car or curbing impulse buying, but face challenges with current apps. Most platforms offer limited features, forcing users to juggle multiple apps, increasing effort and reducing effectiveness.

This chanelled my focus on the need for an integrated solution that simplifies financial tracking, consolidates features, reduces fragmentation and helps users' long-term financial objectives.

Survey insights revealed that young individuals track expenses for specific financial goals, like saving for a car or curbing impulse buying, but face challenges with current apps. Most platforms offer limited features, forcing users to juggle multiple apps, increasing effort and reducing effectiveness.

This chanelled my focus on the need for an integrated solution that simplifies financial tracking, consolidates features, reduces fragmentation and helps users' long-term financial objectives.

MARKET TREND

Rising popularity of using digital tracking apps.

These apps along with digital payment apps store fragmented data.

CONSTRAITS

Forgetting to track transactions immediately after each payment. Sounds humanly impossible to be on top of it right?!

GAP in FINANCIAL LITERACY

According to a study conducted in 2023 by National Institute of Securities Markets (NISM), only 24% Indians are financially literate.

This also points out a need for better financial learning to promote better financial decision-making

CONSTRAITS

Payment through different sources and means

The Path Forward...

The Path Forward...

Recognizing the gap in storing data and having it accessible at the tip of one’s finger, the focus was on providing a service which bridges this gap with a positive experience.

There are mainly two focus areas within this concept-

consolidating fragmented data on different apps to one place; possibly integrate the system with an existing app

providing insights on financial strengths and weaknesses. provide useful adivce based on the insights

ease of access

increased efficiency of tracking

reduce the number of apps

consolidating fragmented data on different apps to one place; possibly integrate the system with an existing app

ease of access

increased efficiency of tracking

reduce the number of apps

improve and influence decision making

reminders and alerts to reinforce certain behaviour

providing insights on financial strengths and weaknesses. provide useful adivce based on the insights

improve and influence decision making

reminders and alerts to reinforce certain behaviour

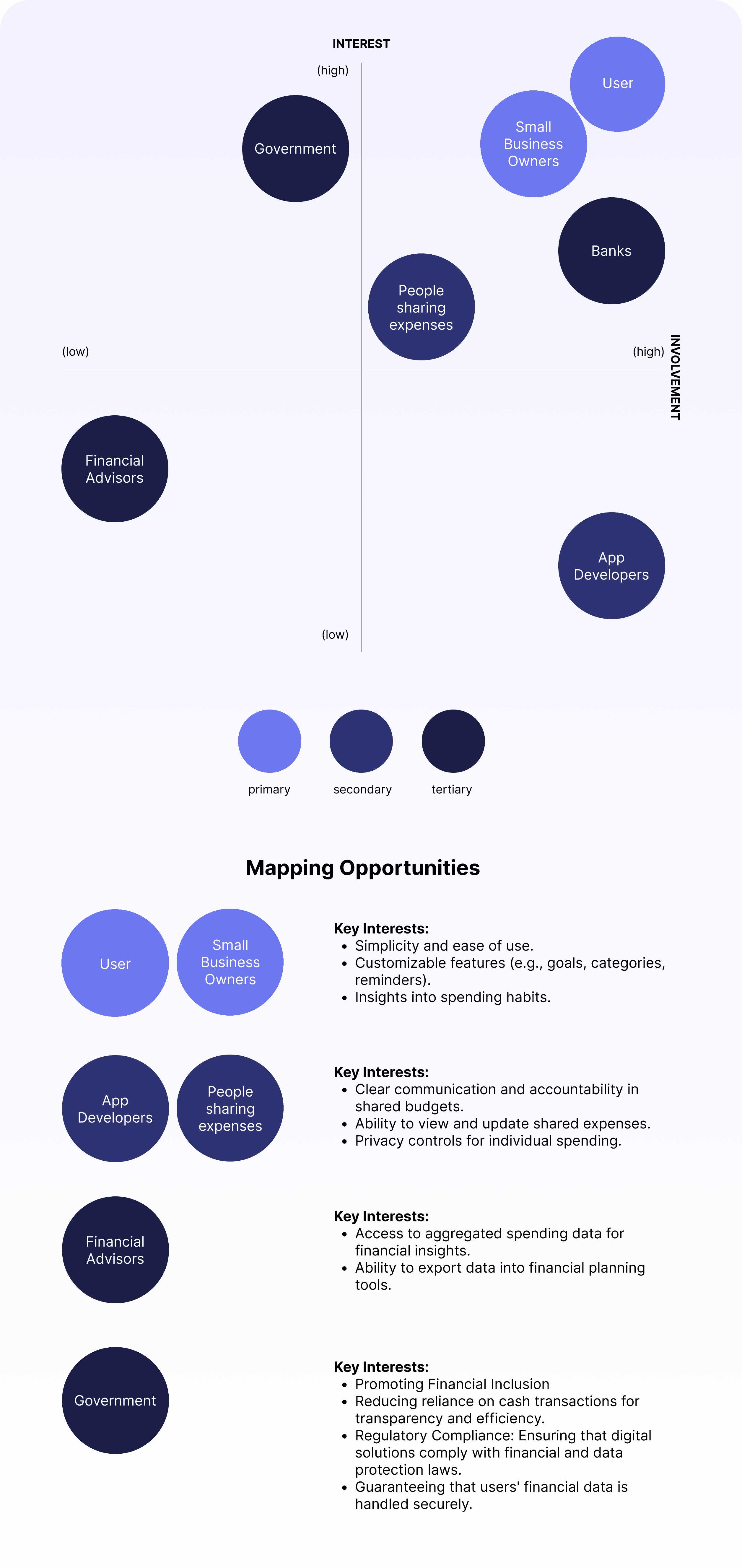

Stakeholder Analysis

Stakeholder Analysis

After funneling down what needs to be done, I moved my focus to understand who the key players are and how will they be affected by the project and vice versa.

After funneling down what needs to be done, I moved my focus to understand who the key players are and how will they be affected by the project and vice versa.

INTEREST

(high)

(low)

(high)

(low)

INVOLVEMENT

Small Business Owners

App Developers

Financial Advisors

Government

Banks

People sharing expenses

User

primary

secondary

tertiary

Mapping Opportunities

User

Small Business Owners

Key Interests:

Simplicity and ease of use.

Customizable features (e.g., goals, categories, reminders).

Insights into spending habits.

App Developers

People sharing expenses

Key Interests:

Clear communication and accountability in shared budgets.

Ability to view and update shared expenses.

Privacy controls for individual spending.

Financial Advisors

Key Interests:

Access to aggregated spending data for financial insights.

Ability to export data into financial planning tools.

Government

Key Interests:

Promoting Financial Inclusion

Reducing reliance on cash transactions for transparency and efficiency.

Regulatory Compliance: Ensuring that digital solutions comply with financial and data protection laws.

Guaranteeing that users' financial data is handled securely.

Affinity Map

Affinity Map

Tracking methods & Bugdeting frustrations

Tracking methods & Bugdeting frustrations

want reminders as it is a difficult task to log all transactions without forgetting.

want reminders as it is a difficult task to log all transactions without forgetting.

it is important to get analysis and insights from all the logs.

it is important to get analysis and insights from all the logs.

it is important to get analysis and insights from all the logs.

it is important to get analysis and insights from all the logs.

it would be good to track through bills.

it would be good to track through bills.

Shared Expenses

Easy reminders and keeping a history for clarification even after it's settled. splitwise doesn’t keep a log after settling group expenses

calculations are cognitively heavy, would like something with lesser calculations

Desired features

automated entries

timely reminders

widgets for easy view

alerts for exceeding budget limit

recurring expense tracking system

extensive category list

would like to have app integration with payment apps

03

Building Blocks

03

Building Blocks

Brainstorming

Brainstorming

The solution is designed in phases. It is an added feature to an already existing, well-functioning app instead of building a whole app altogether. This decision was fueled by insights gained from the research. The apps on our phone are ever-increasing and users find it an inconvenience to have to download new and newer apps for every single task.

The solution is designed in phases. It is an added feature to an already existing, well-functioning app instead of building a whole app altogether. This decision was fueled by insights gained from the research. The apps on our phone are ever-increasing and users find it an inconvenience to have to download new and newer apps for every single task.

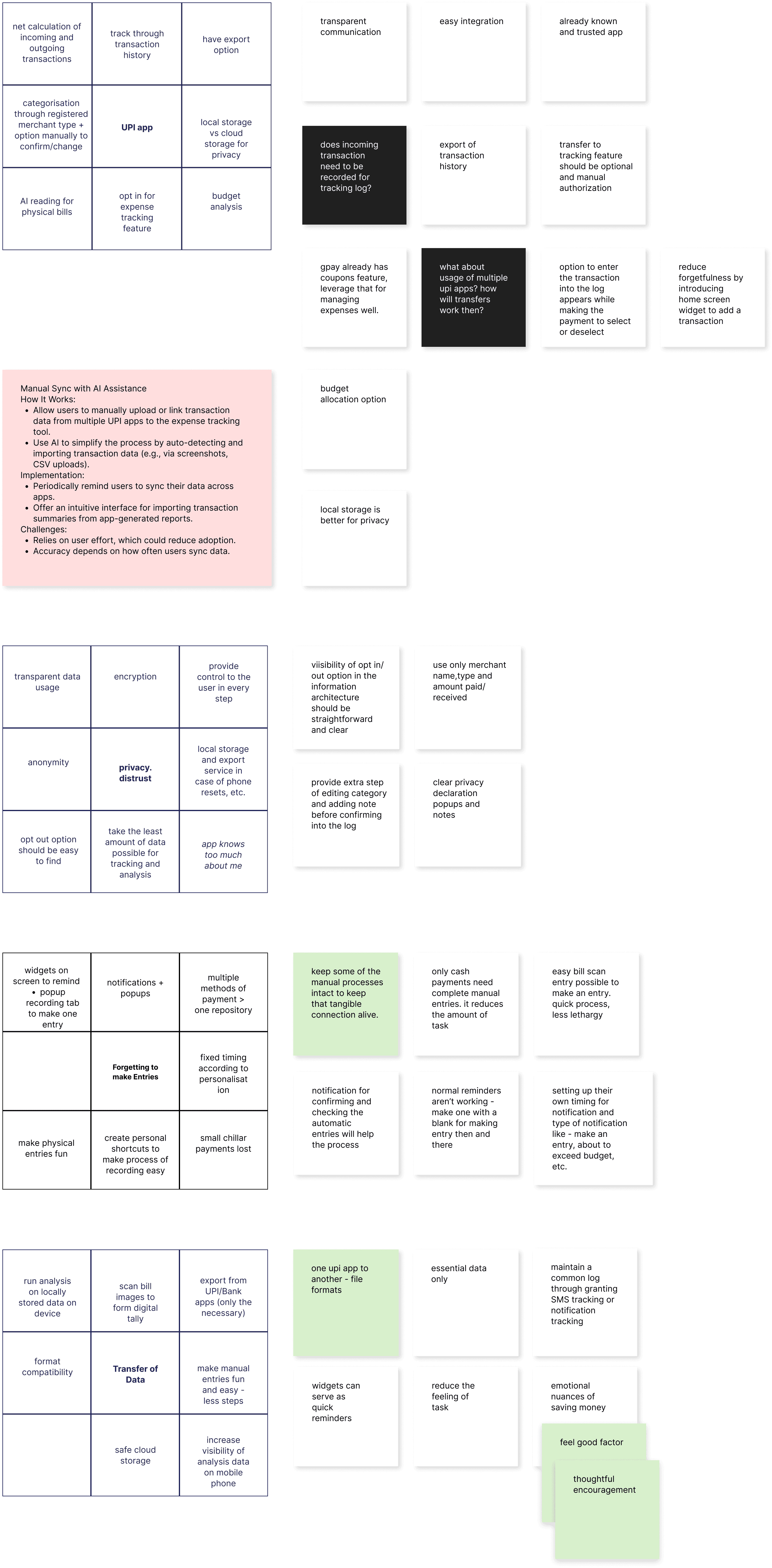

Lotus Diagram

Lotus Diagram

UPI app

tracking apps

tangible vs intangible

privacy. distrust

Forgetting to make Entries

Transfer of Data

TRACKING EXPENSES

Shared Expenses and Bills

Transfer of Data

scan bill images to form digital tally

run analysis on locally stored data on device

format compatibility

export from UPI/Bank apps (only the necessary)

make manual entries fun and easy - less steps

increase visibility of analysis data on mobile phone

safe cloud storage

tracking apps

offer analysis of expenses

extensive categorisation options

link with online payment apps (what about data laws?)

quick balance check before payment at places

analysis report exportable as .xlsx

manual entries + import from online transactions apps

widgets on screen for reminders and advice

budget allocation

Forgetting to make Entries

notifications + popups

multiple methods of payment > one repository

fixed timing according to personalisation

create personal shortcuts to make process of recording easy

make physical entries fun

widgets on screen to remind

popup recording tab to make one entry

small chillar payments lost

tangible vs intangible

detachment from online transfers

implusive purchases increase

remind twice thrice once limit exceeds on payment window

make the user feel even on digital platform

cultural nuances like baunhi

the feeling of payment in cash makes one remember

show graphic representation of money on digital app

tips and conventions

provide praises on doing good, achieving budget, incentivise

remind twice thrice once limit exceeds on payment window

recent updates on financial news like laws and scams

interesting and short. no one reads long stuff

credibility of source of information

provide advice upon analysis

set goals to achieve

privacy. distrust

encryption

provide control to the user in every step

local storage and export service in case of phone resets, etc.

opt out option should be easy to find

anonymity

take the least amount of data possible for tracking and analysis

transparent data usage

app knows too much about me

UPI app

track through transaction history

have export option

local storage vs cloud storage for privacy

opt in for expense tracking feature

AI reading for physical bills

categorisation through registered merchant type + option manually to confirm/change

net calculation of incoming and outgoing transactions

budget analysis

Shared Expenses and Bills

convert manual to digital calculation of shares

frustration

splitwise doesn’t offer unequal split calculation

having record of list of items bought will help sort shared expenses better

integrate with tracking app for easy entry?

payment req. sharing with other members on UPI groups option

my share goes into tracker and others go out

budget allocation

option to enter the transaction into the log appears while making the payment to select or deselect

UPI app

track through transaction history

have export option

local storage vs cloud storage for privacy

opt in for expense tracking feature

AI reading for physical bills

categorisation through registered merchant type + option manually to confirm/change

net calculation of incoming and outgoing transactions

budget analysis

transparent communication

easy integration

already known and trusted app

does incoming transaction need to be recorded for tracking log?

export of transaction history

transfer to tracking feature should be optional and manual authorization

option to enter the transaction into the log appears while making the payment to select or deselect

gpay already has coupons feature, leverage that for managing expenses well.

what about usage of multiple upi apps? how will transfers work then?

reduce forgetfulness by introducing home screen widget to add a transaction

budget allocation option

local storage is better for privacy

Manual Sync with AI Assistance

How It Works:

Allow users to manually upload or link transaction data from multiple UPI apps to the expense tracking tool.

Use AI to simplify the process by auto-detecting and importing transaction data (e.g., via screenshots, CSV uploads).

Implementation:

Periodically remind users to sync their data across apps.

Offer an intuitive interface for importing transaction summaries from app-generated reports.

Challenges:

Relies on user effort, which could reduce adoption.

Accuracy depends on how often users sync data.

widgets can serve as quick reminders

reduce the feeling of task

emotional nuances of saving money

feel good factor

thoughtful encouragement

maintain a common log through granting SMS tracking or notification tracking

one upi app to another - file formats

essential data only

Transfer of Data

scan bill images to form digital tally

run analysis on locally stored data on device

format compatibility

export from UPI/Bank apps (only the necessary)

make manual entries fun and easy - less steps

increase visibility of analysis data on mobile phone

safe cloud storage

Forgetting to make Entries

notifications + popups

multiple methods of payment > one repository

fixed timing according to personalisation

create personal shortcuts to make process of recording easy

make physical entries fun

widgets on screen to remind

popup recording tab to make one entry

small chillar payments lost

keep some of the manual processes intact to keep that tangible connection alive.

easy bill scan entry possible to make an entry. quick process, less lethargy

setting up their own timing for notification and type of notification like - make an entry, about to exceed budget, etc.

notification for confirming and checking the automatic entries will help the process

only cash payments need complete manual entries. it reduces the amount of task

normal reminders aren’t working - make one with a blank for making entry then and there

anonymity

opt out option should be easy to find

local storage and export service in case of phone resets, etc.

app knows too much about me

privacy. distrust

take the least amount of data possible for tracking and analysis

encryption

provide control to the user in every step

transparent data usage

viisibility of opt in/out option in the information architecture should be straightforward and clear

use only merchant name,type and amount paid/received

provide extra step of editing category and adding note before confirming into the log

clear privacy declaration popups and notes

Integrate budgeting and tracking dashboard in a UPI app

existing familiarity

transaction log present

categorisation present

sensitive data - privacy concerns

distrust towards an app that knows too much about one’s expenses

payments are divided across multiple UPI apps

overcrowding of features

Build a new app for easy collaborative tracking across different methods of payments

integrate tracking as an feature in an existing expense tracker app

3 pathways

Pros

Cons

user-friendly UI from scratch

higher trust can be built

work across all UPI apps

personal financing can be expanded

difficult onboarding

development from scratch

feature creep

Pros

Cons

familiarity with app

no additional app building

upgrade basic to better version

competitive differentiation

wide user base already

feature creep

overlap of data while transferring from other apps

Pros

Cons

3 pathways

Build a new app for easy collaborative tracking across different methods of payments

user-friendly UI from scratch

higher trust can be built

work across all UPI apps

personal financing can be expanded

difficult onboarding

development from scratch

feature creep

Pros

Cons

Integrate budgeting and tracking dashboard in a UPI app

existing familiarity

transaction log present

categorisation present

sensitive data - privacy concerns

distrust towards an app that knows too much about one’s expenses

payments are divided across multiple UPI apps

overcrowding of features

Pros

Cons

integrate tracking as an feature in an existing expense tracker app

familiarity with app

no additional app building

upgrade basic to better version

competitive differentiation

wide user base already

feature creep

overlap of data while transferring from other apps

Pros

Cons

Presenting...

Presenting...

Track-a-thon

Track-a-thon

A solution designed to simplify daily financial management by integrating UPI transaction data with a tracking app that provides extensive analysis. It offers seamless insights across multiple payment apps, enabling users to set goals, track budgets, and gain actionable spending insights, all through an intuitive financial UX.

A solution designed to simplify daily financial management by integrating UPI transaction data with a tracking app that provides extensive analysis. It offers seamless insights across multiple payment apps, enabling users to set goals, track budgets, and gain actionable spending insights, all through an intuitive financial UX.

04

04

Final Construction & Testing

Final Construction & Testing

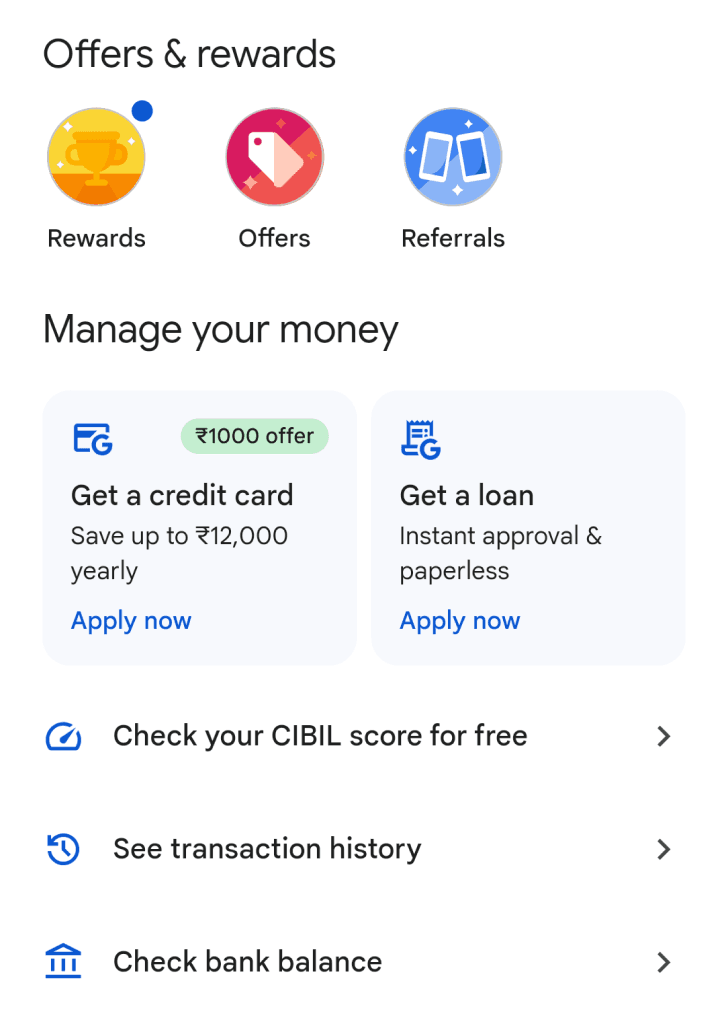

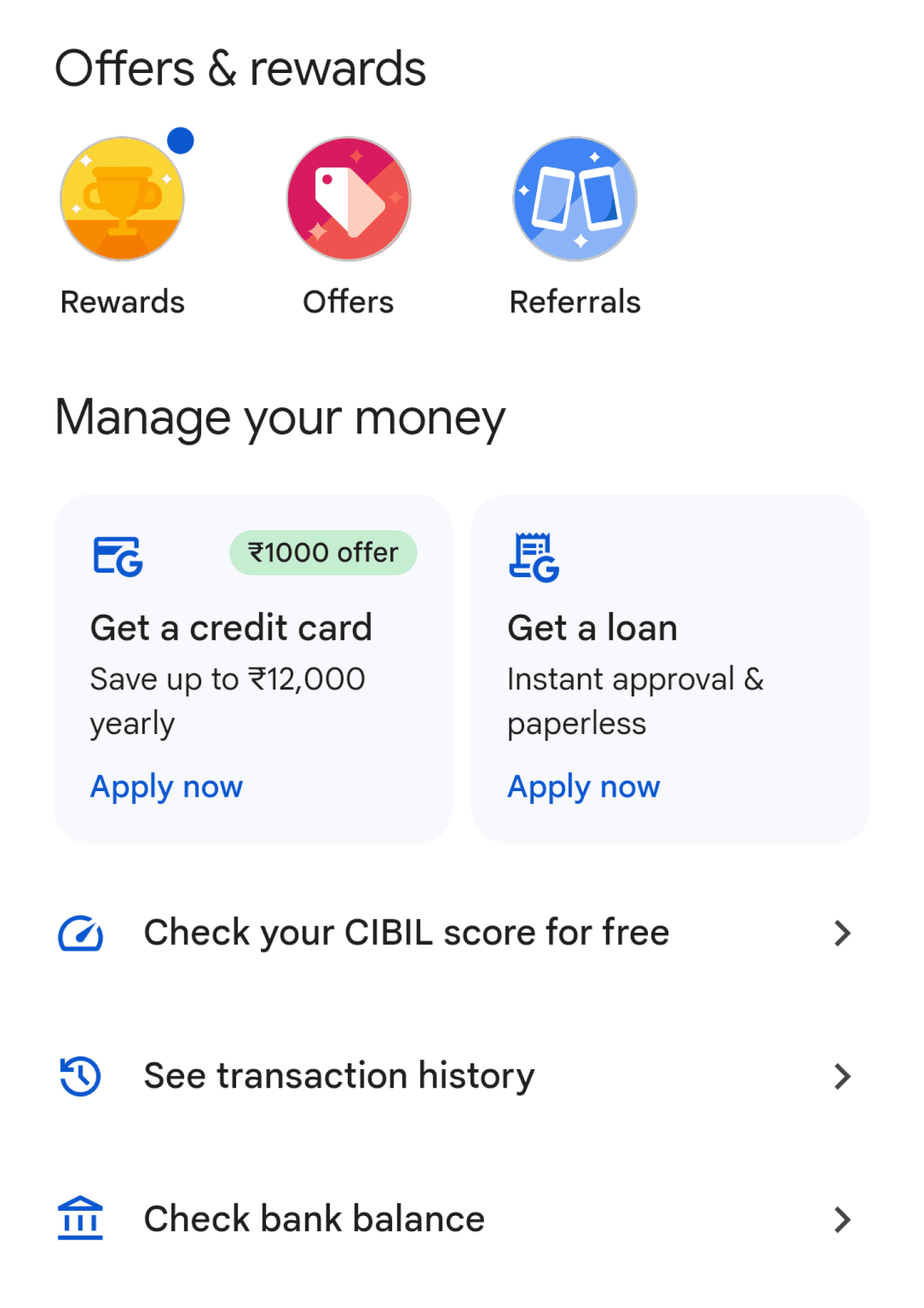

First step of the strategy involves including an export feature in a UPI payment app like GooglePay (GPay).

Transaction History Export

01

Key Features

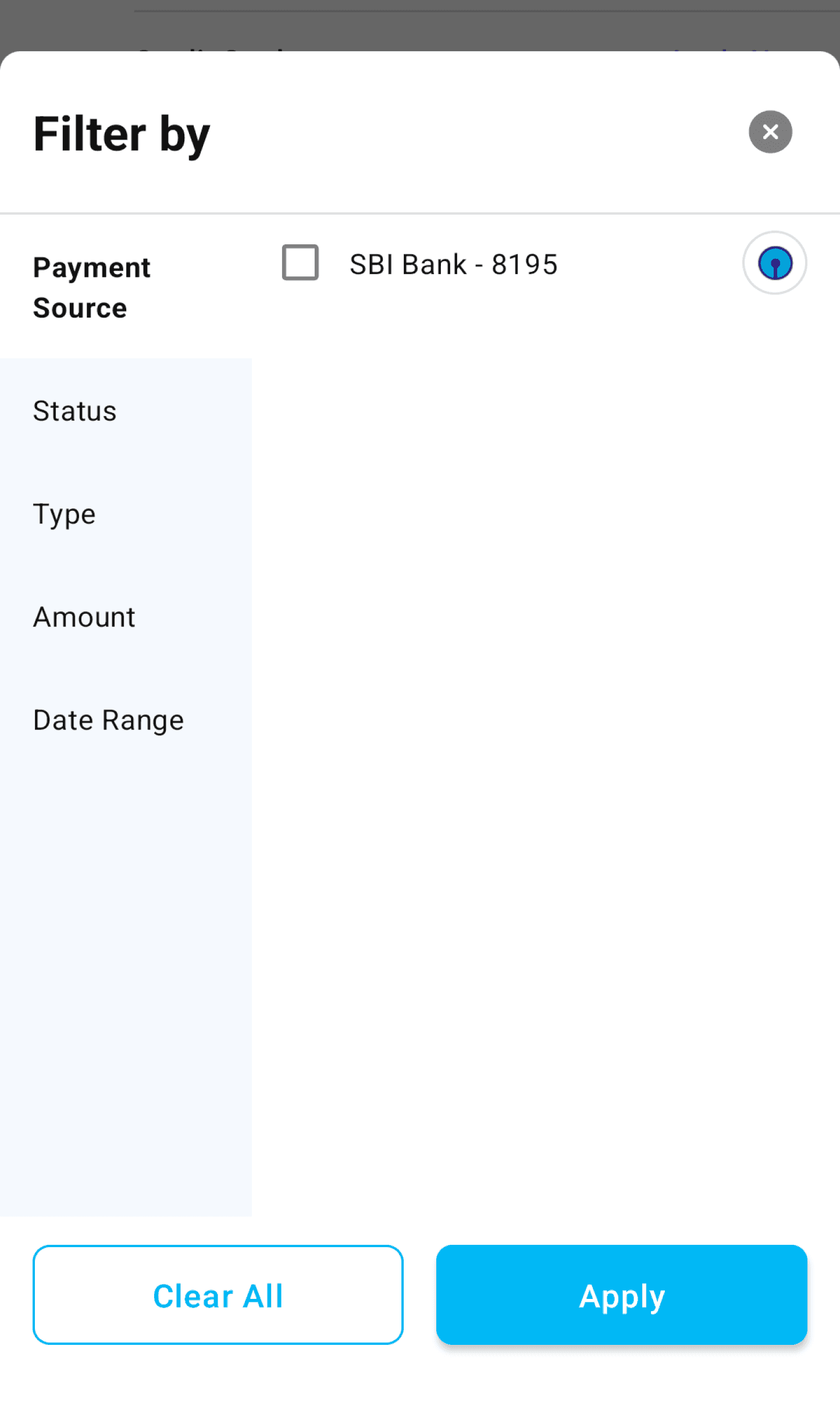

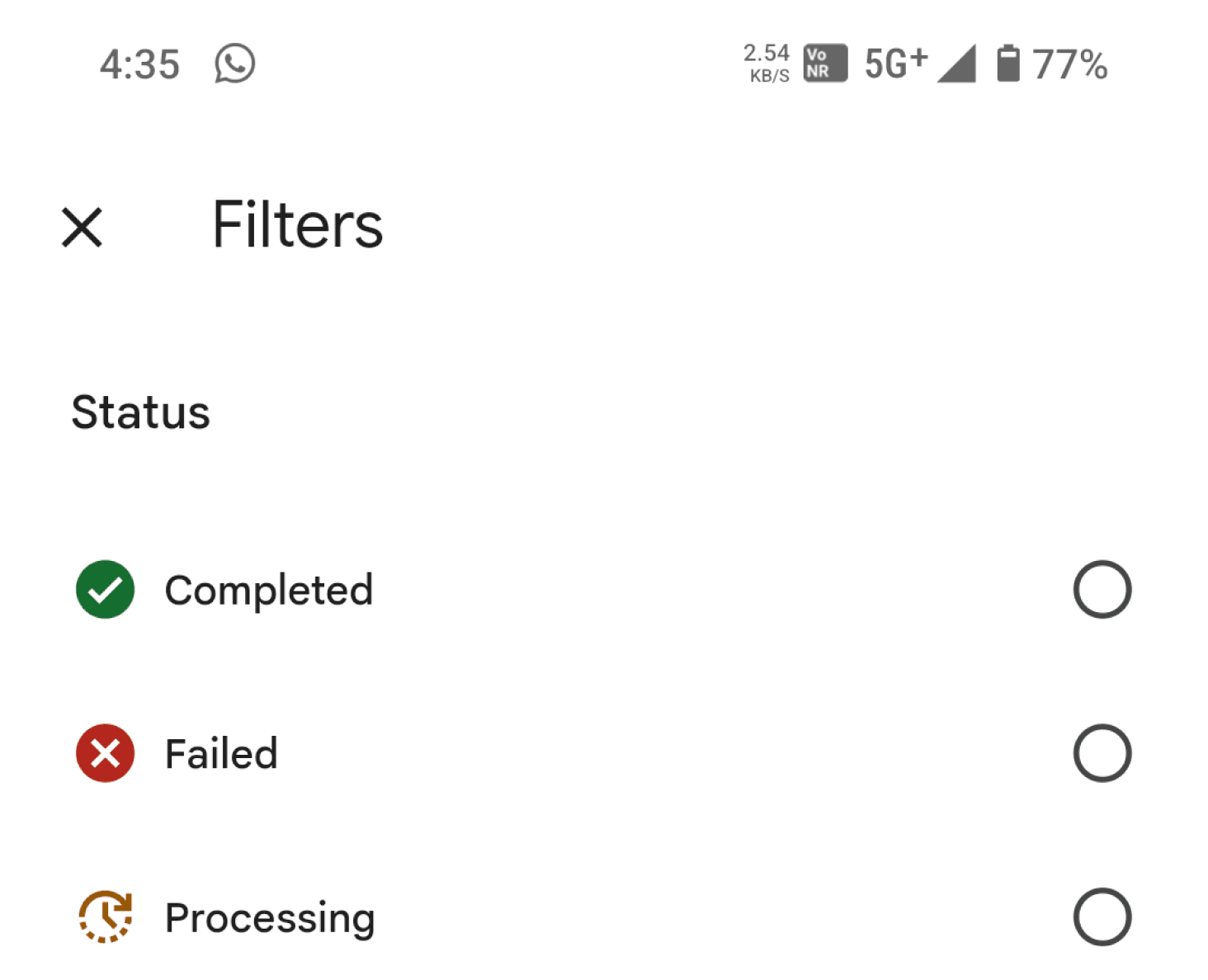

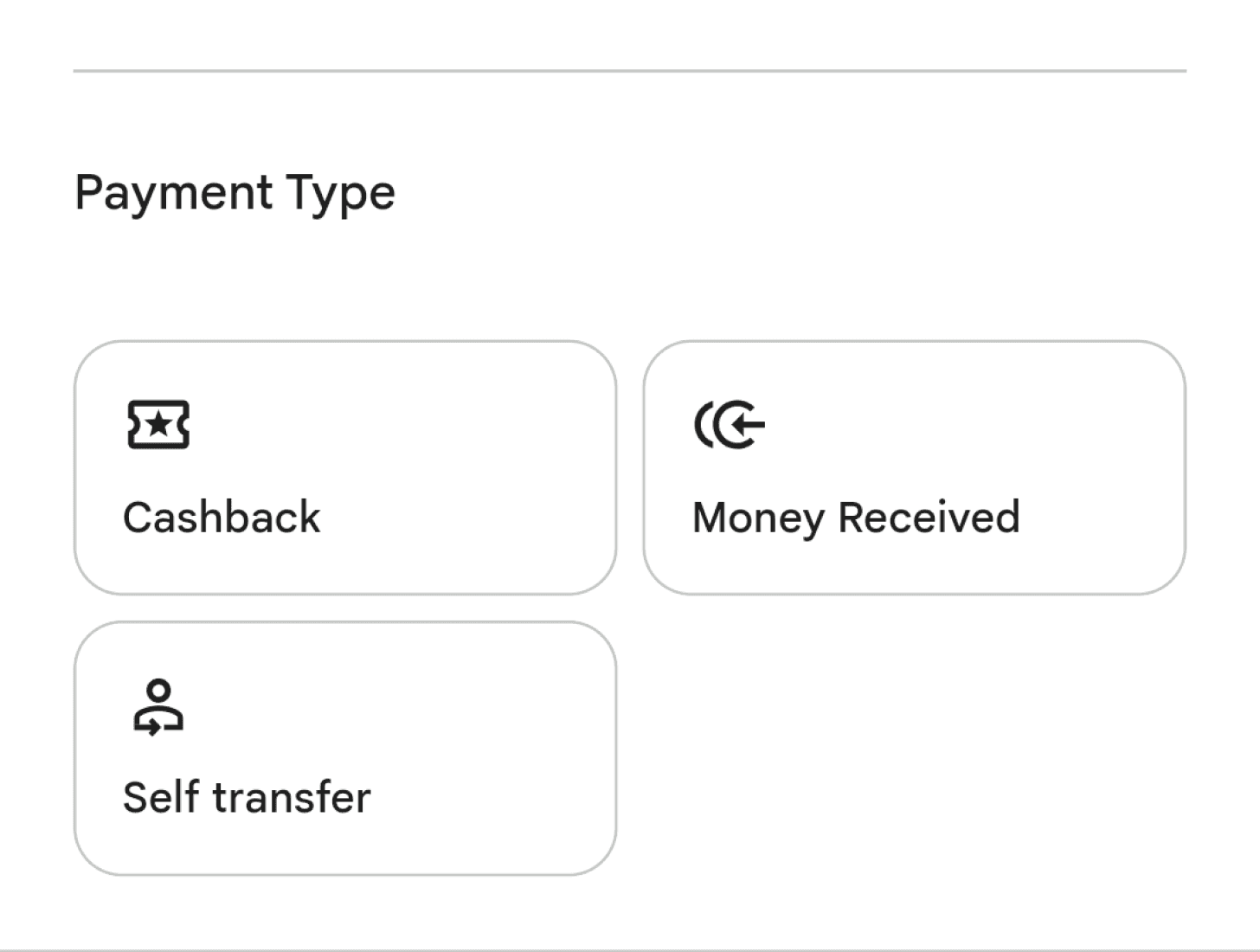

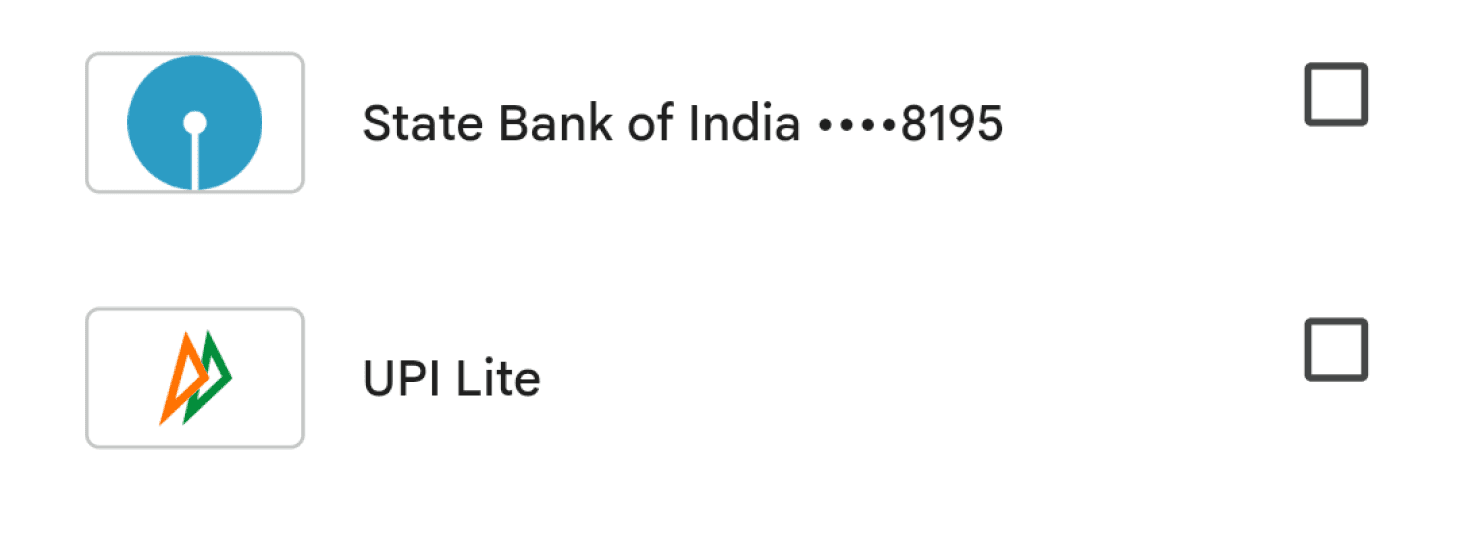

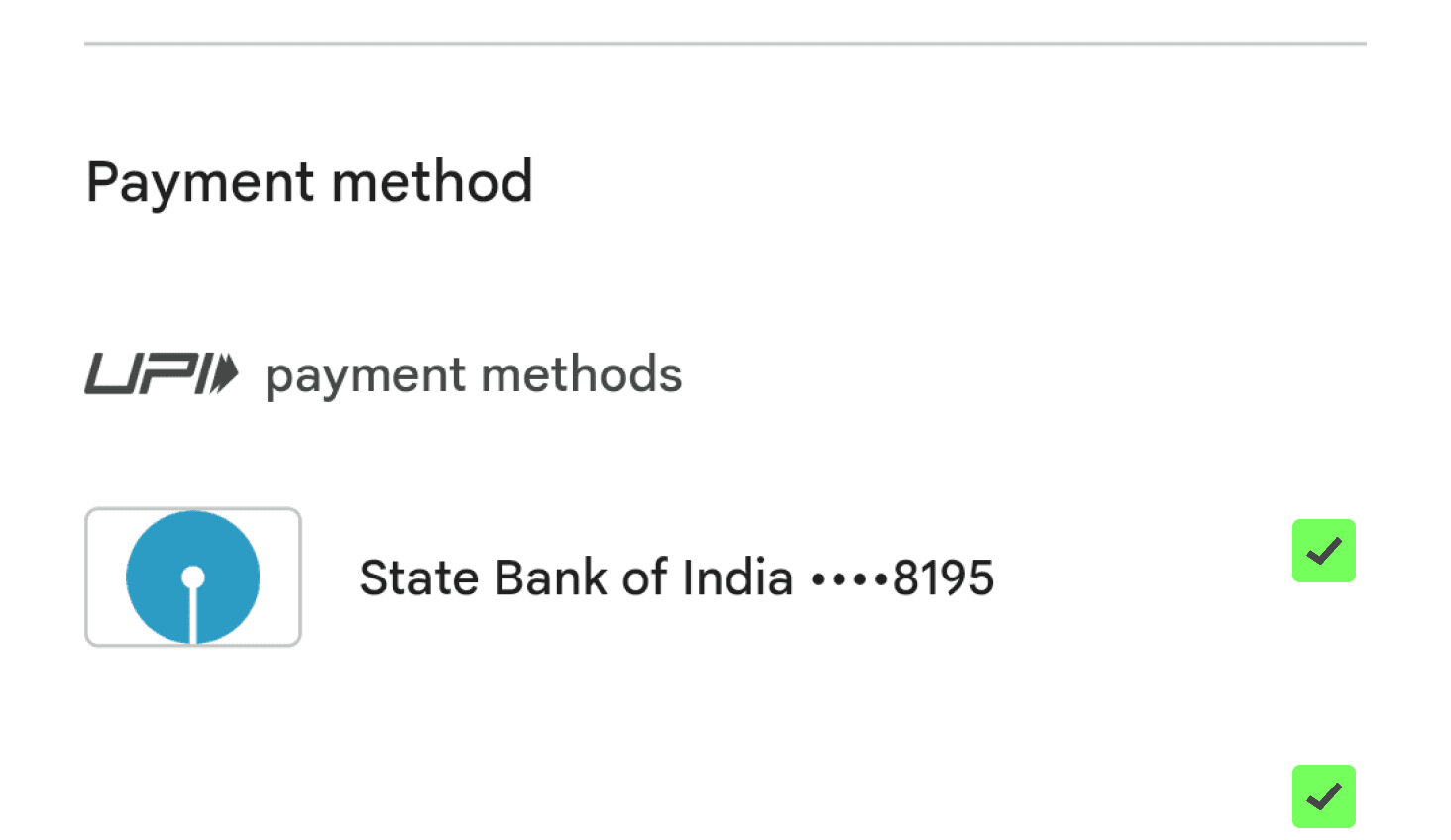

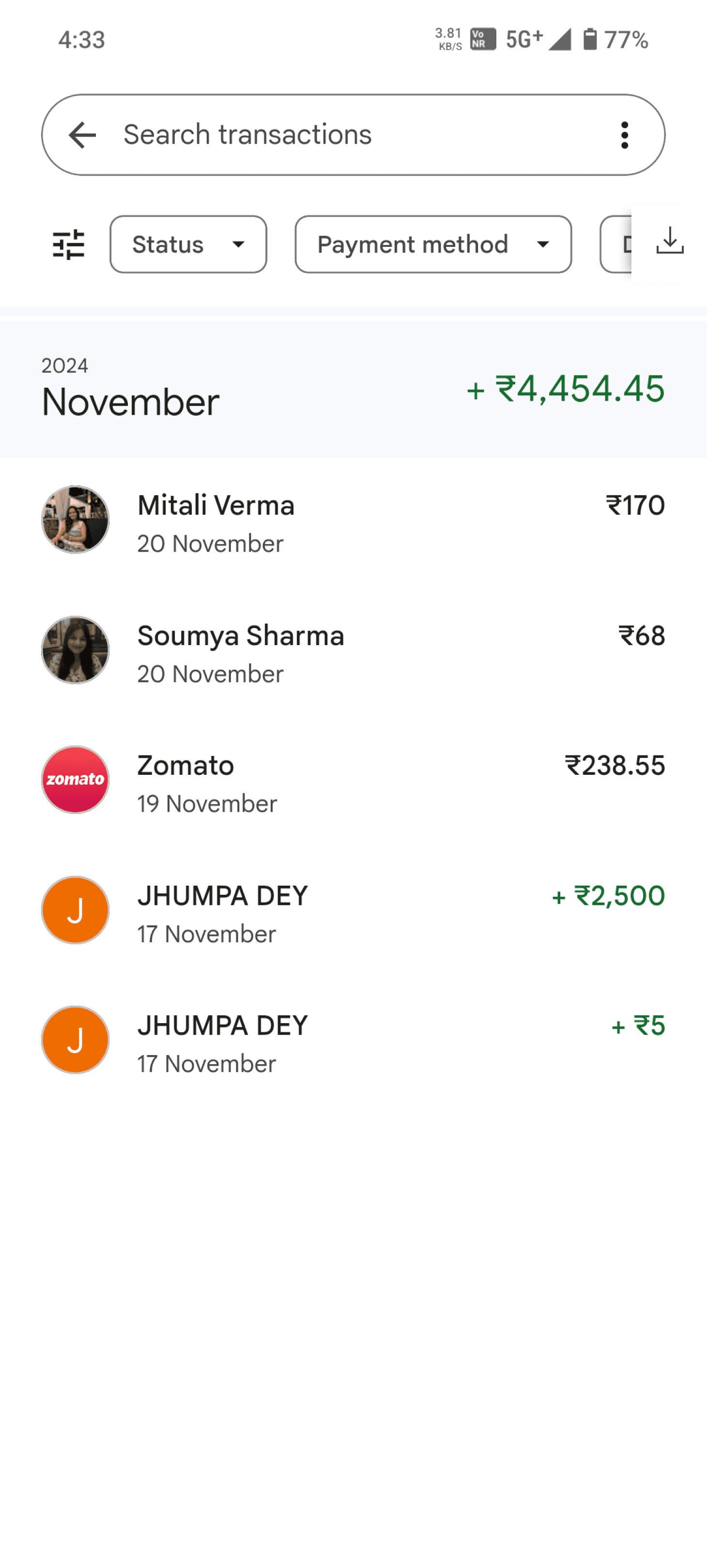

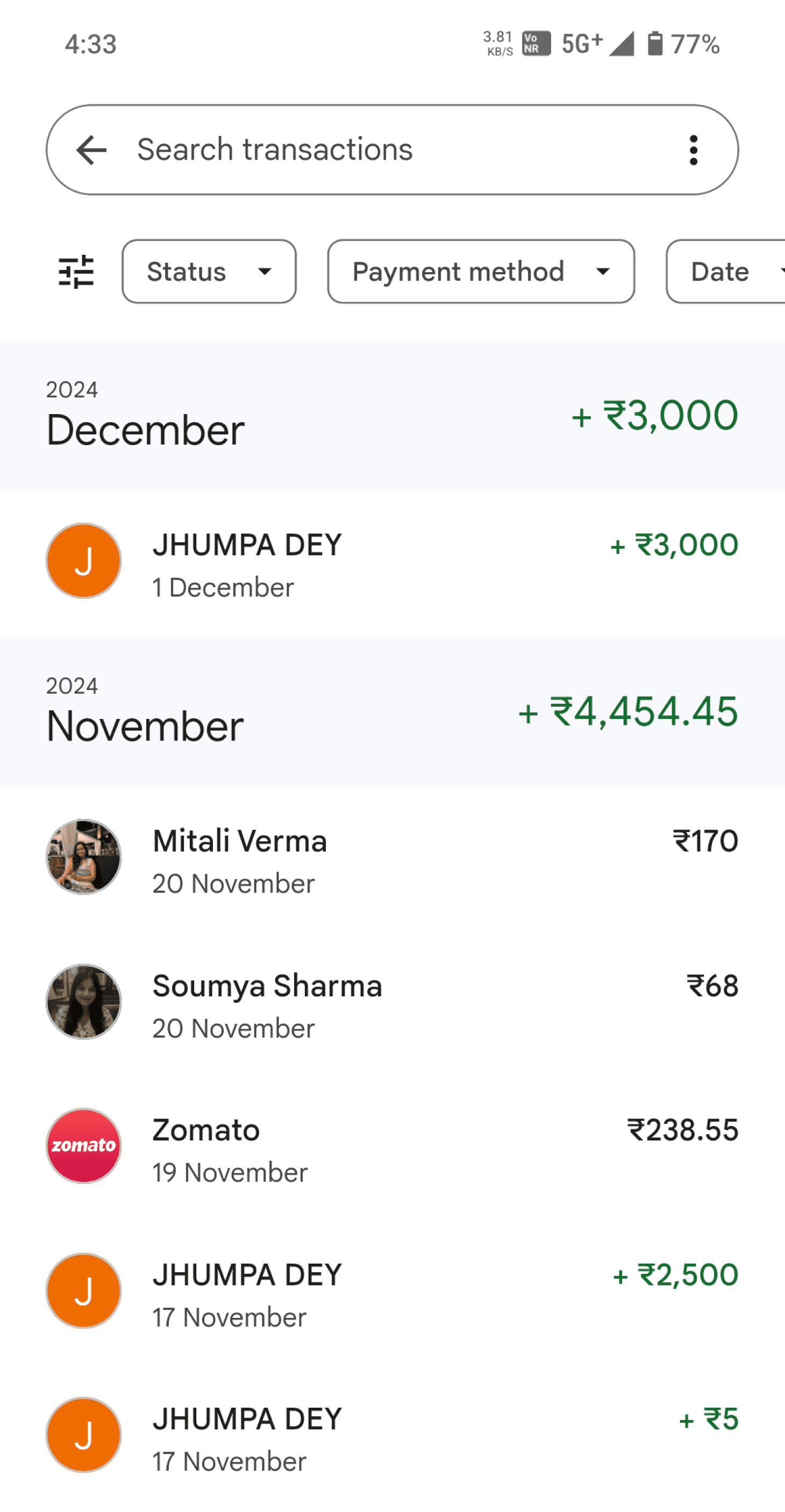

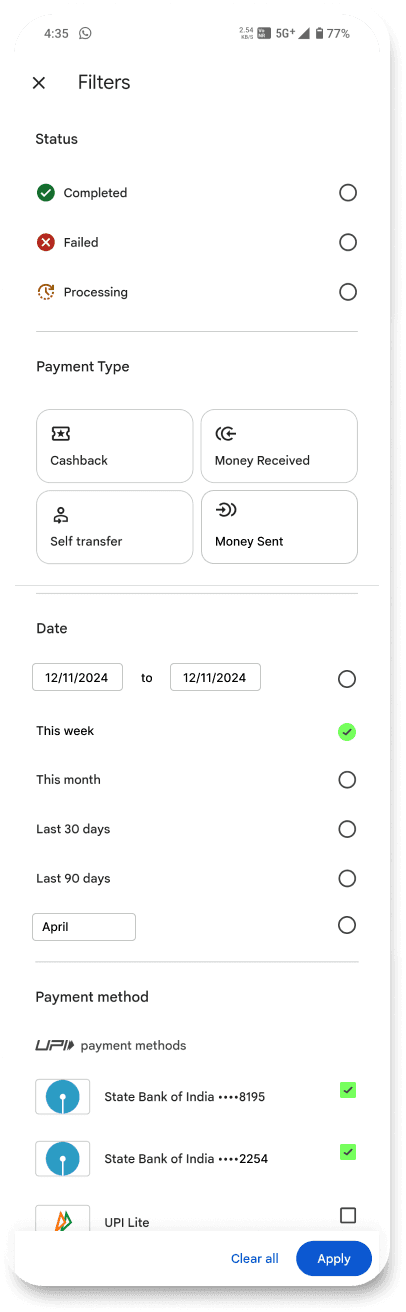

After having applied the desired filters on date, payment type and method, the user can now export it conveniently in formats compatible with multiple devices.

User Flow: Export a compatible excel file from payment app

WHY would Gpay want to introduce this feature?

User Retention:

Offering value-added features such as seamless data export enhances user engagement and loyalty.

Brand Differentiation: This feature can differentiate the app from competitors lacking integration capabilities.

Ecosystem Play: Collaboration with personal finance apps can position the UPI app as part of a broader financial management ecosystem.

Partnership Revenue: Monetize collaborations through commissions or shared revenues with finance apps.

More filters allow the user to export transactions as per their control and gives more control over what they want to export.

Modified filters to increase choices of personalised information transfer

Money Sent

This week

April

12/11/2024

to

12/11/2024

2254

Transactions based on filters

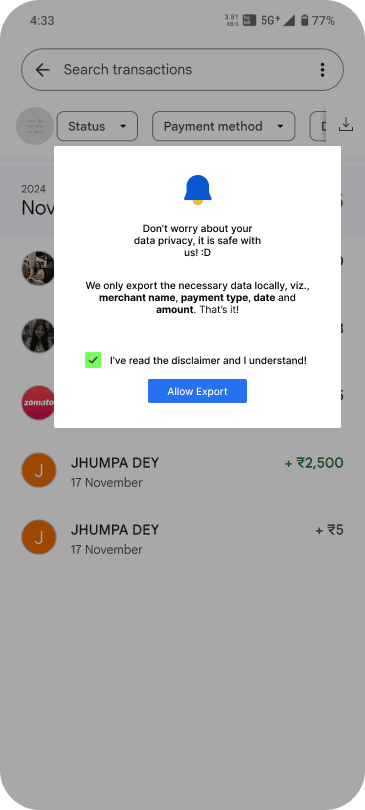

Clear privacy declarations about locally stored data upon allowing

Don’t worry about your data privacy, it is safe with us! :D

We only export the necessary data locally, viz., merchant name, payment type, date and amount. That’s it!

Allow Export

I’ve read the disclaimer and I understand!

The export function is easy to incorporate as filters are already present and require minimal modifications.

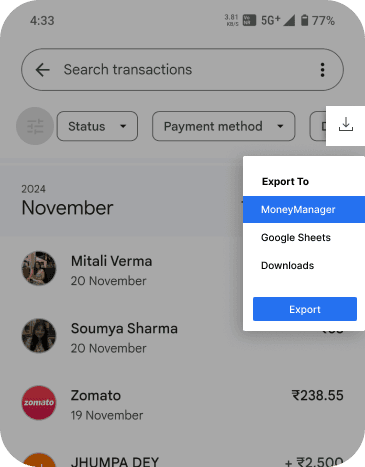

The Export To feature links to various compatible formats in apps detected on the phone.

The most common type of file export formats are .pdf, .csv, .tsv and .xlsx

Export To

MoneyManager

Google Sheets

Downloads

Export

Suggested Way of Export

Information Architecture

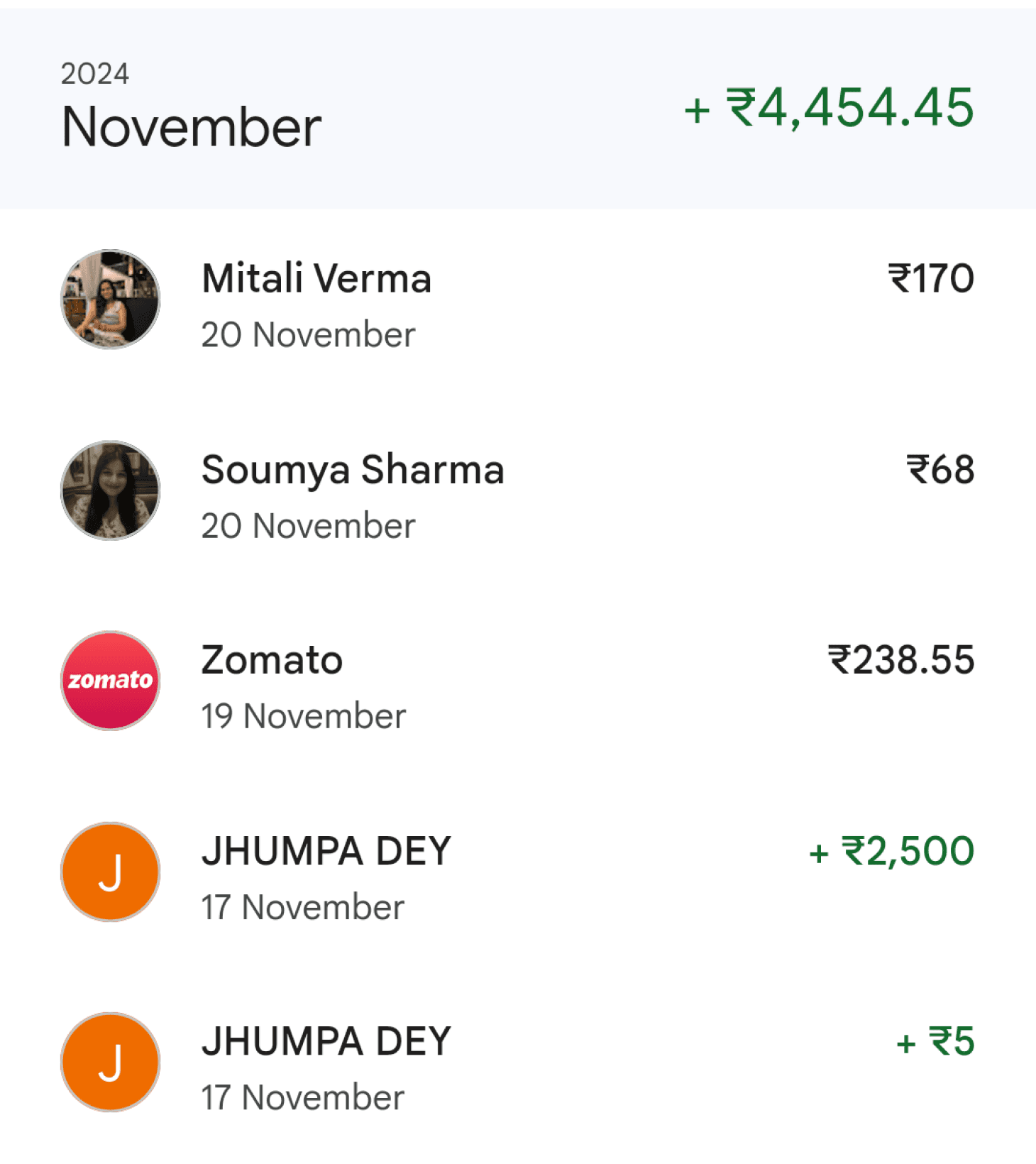

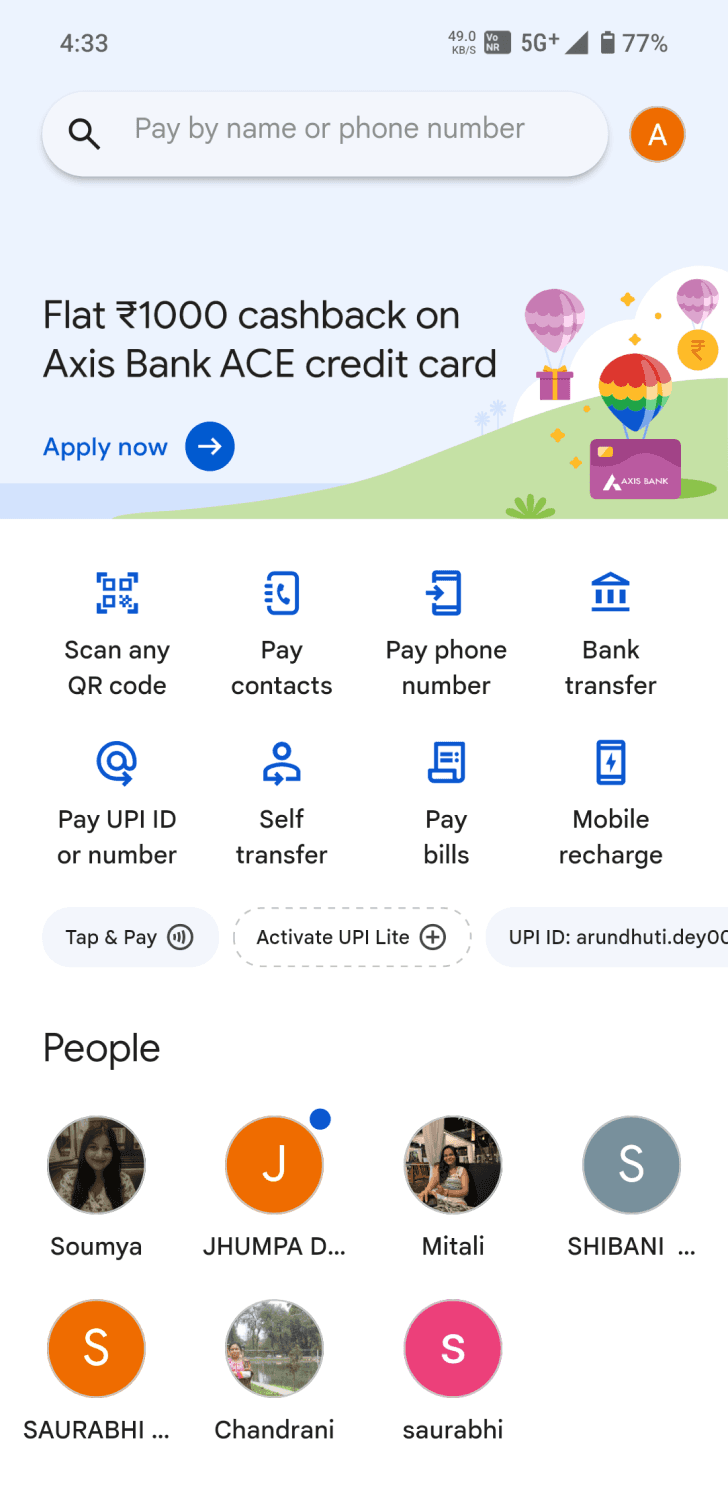

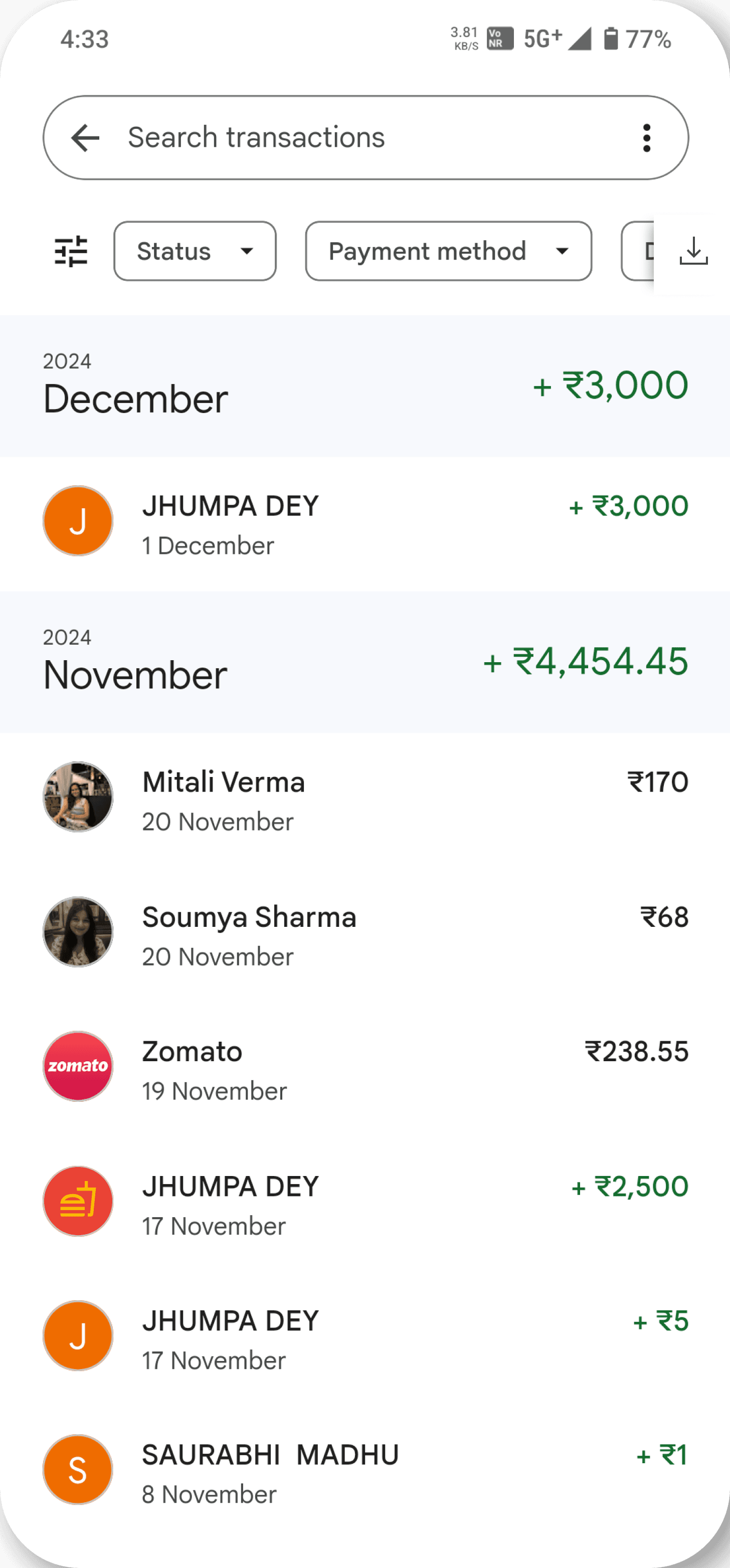

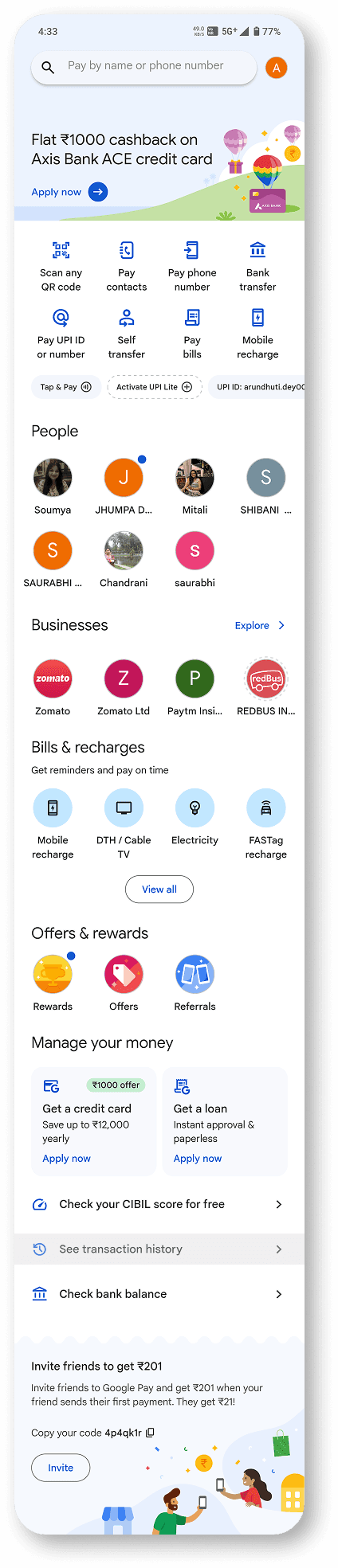

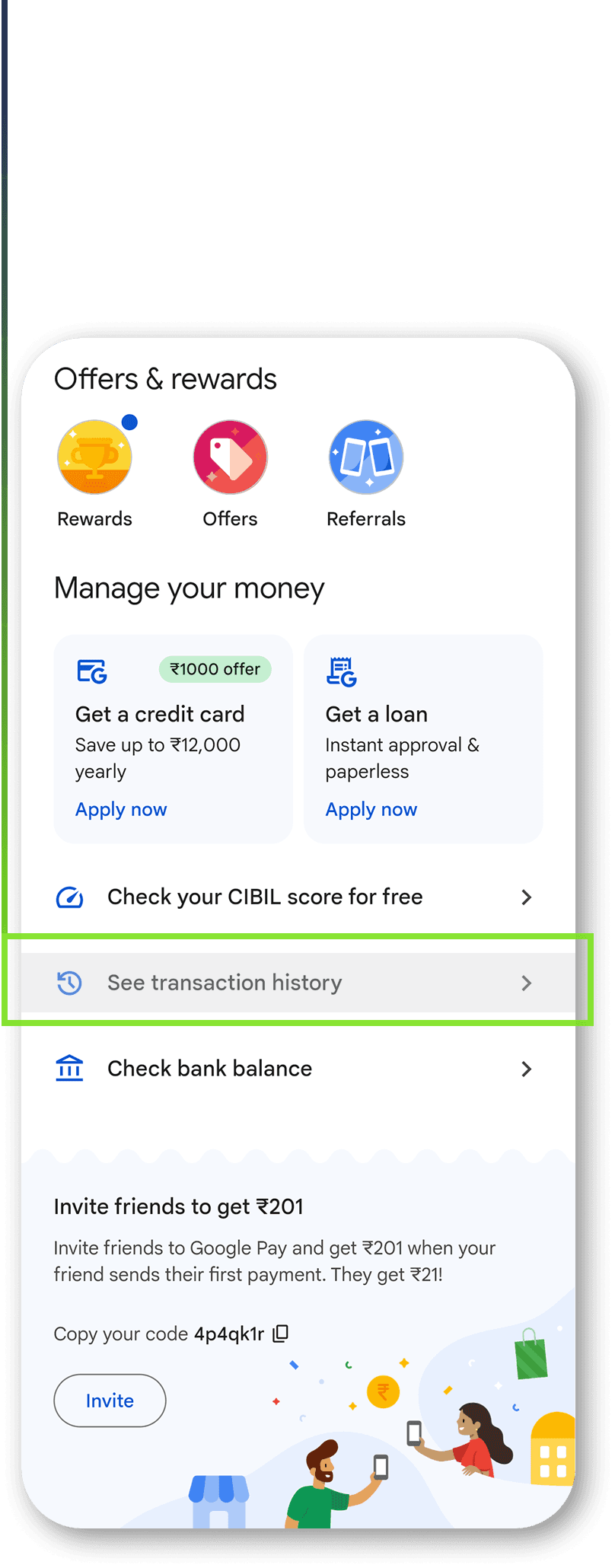

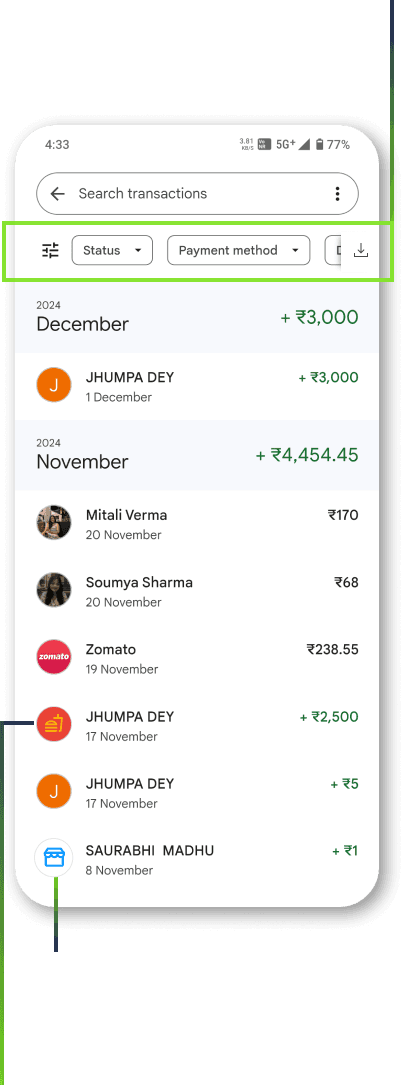

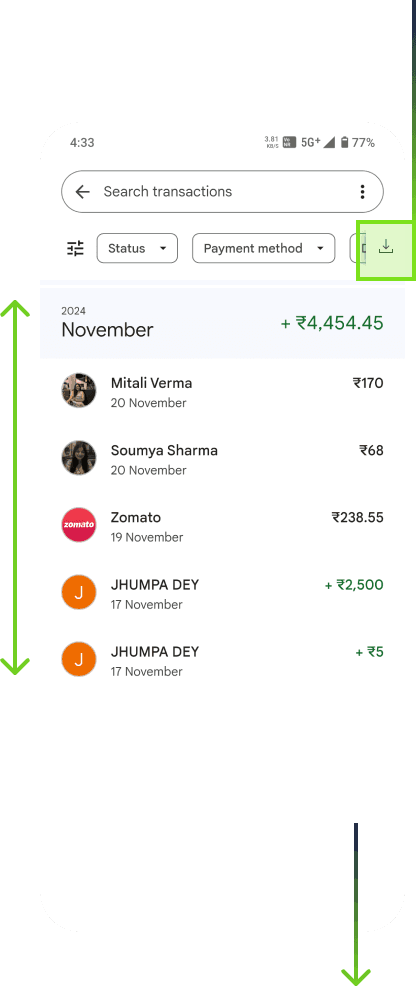

Gpay already has a transaction history with relevant data like date, time, registered merchant type, payment type, payment method, etc.

Available filters to sort and view data can also be used to categorise and export data from the app in a simplified manner.

Merchant registration into categories will help faster and easy recall for users instead of just names

First step of the strategy involves including an export feature in a UPI payment app like GooglePay (GPay).

Transaction History Export

01

Key Features

Gpay already has a transaction history with relevant data like date, time, registered merchant type, payment type, payment method, etc.

Merchant registration into categories will help faster and easy recall for users instead of just names

Modified filters to increase choices of personalised information transfer

After having applied the desired filters on date, payment type and method, the user can now export it conveniently in formats compatible with multiple devices.

Transactions based on filters

Clear privacy declarations about locally stored data upon allowing

The most common type of file export formats are .pdf, .csv, .tsv and .xlsx

User Flow: Export a compatible excel file from payment app

Suggested Way of Export

The export function is easy to incorporate as filters are already present and require minimal modifications.

The Export To feature links to various compatible formats in apps detected on the phone.

WHY would Gpay want to introduce this feature?

User Retention:

Offering value-added features such as seamless data export enhances user engagement and loyalty.

Brand Differentiation: This feature can differentiate the app from competitors lacking integration capabilities.

Ecosystem Play: Collaboration with personal finance apps can position the UPI app as part of a broader financial management ecosystem.

Partnership Revenue: Monetize collaborations through commissions or shared revenues with finance apps.

Available filters to sort and view data can also be used to categorise and export data from the app in a simplified manner.

Information Architecture

More filters allow the user to export transactions as per their control and gives more control over what they want to export.

According to feedback received from expert,

According to feedback received from expert,

people will enjoy a feel good factor

people will enjoy a feel good factor

what is the USP for the user to come back to the app again and again

what is the USP for the user to come back to the app again and again

emotion of feeling guilty

emotion of feeling guilty looking at expenses

exciting Reward System on completing expense logs coming soon…

exciting Reward System on completing expense logs coming soon…

02

Freemium App

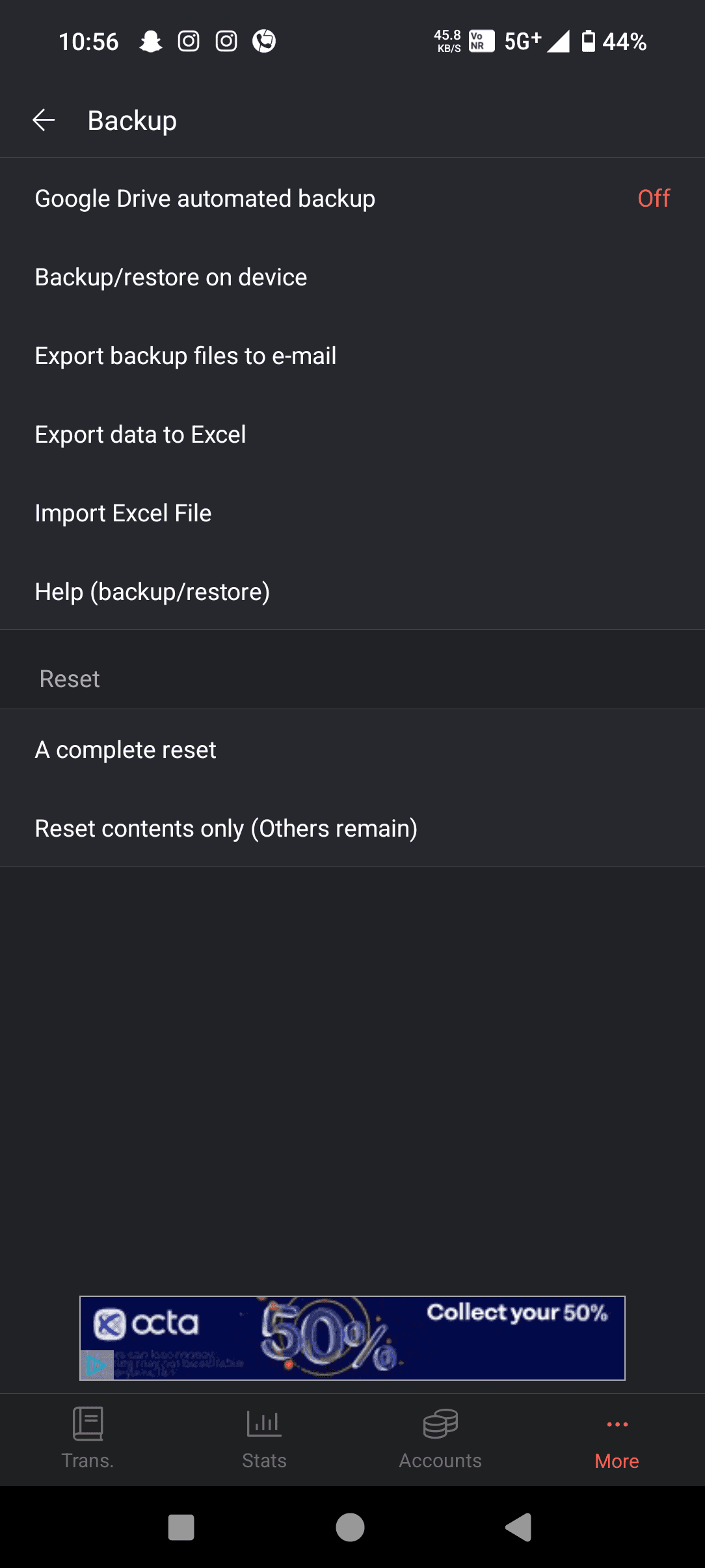

MoneyManager App Integration

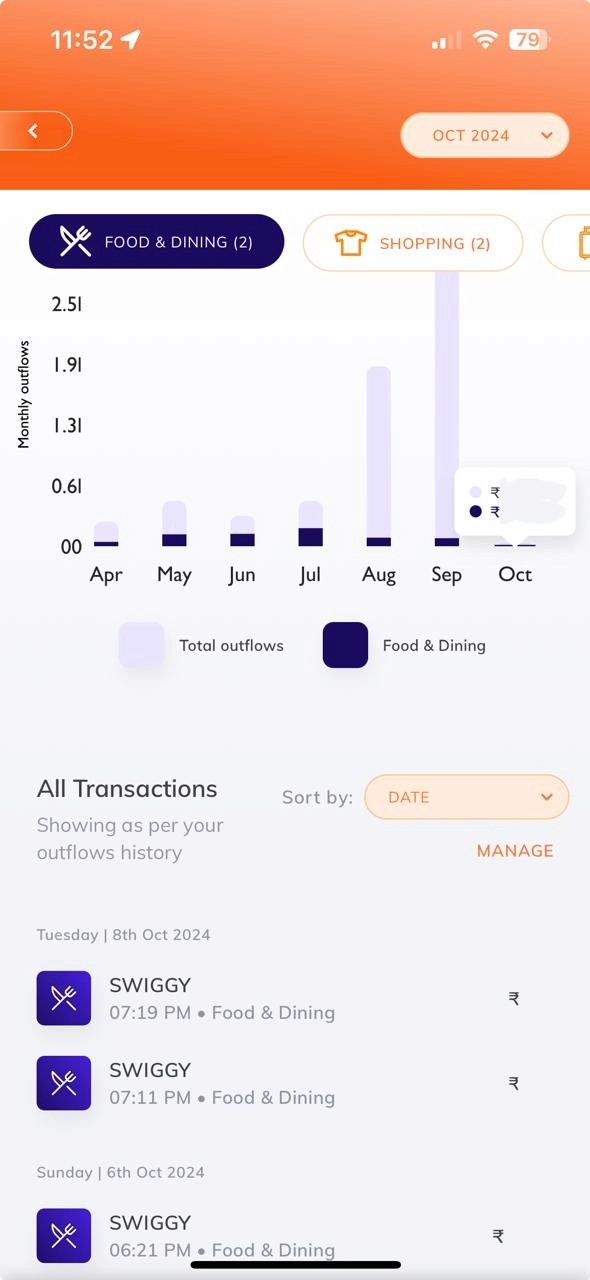

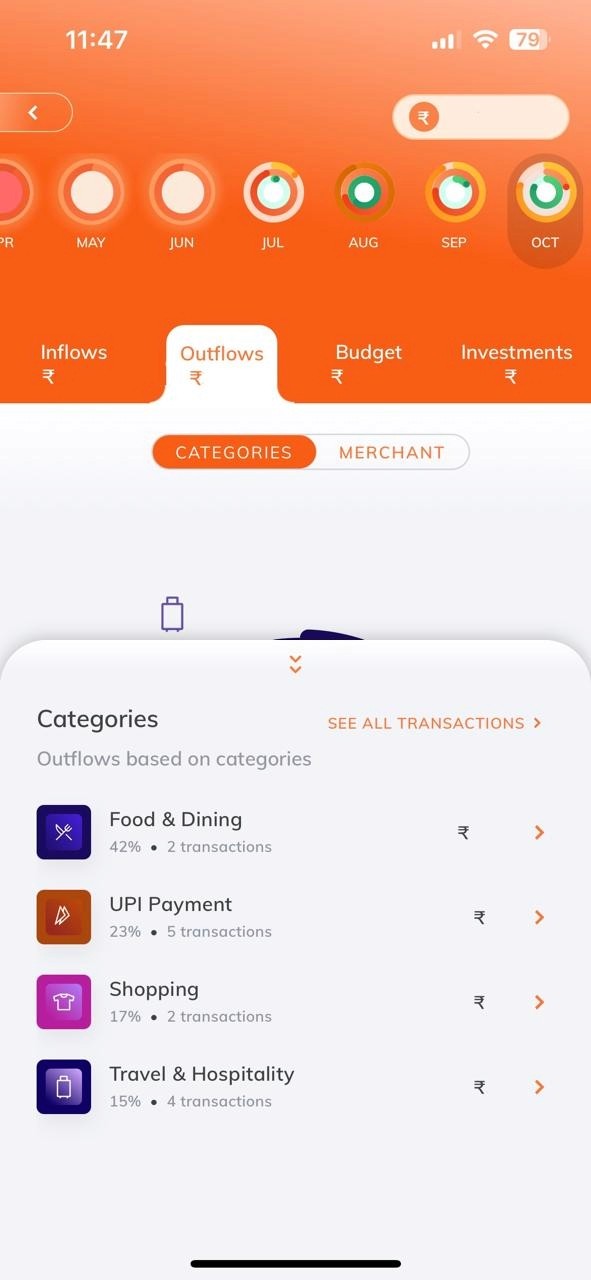

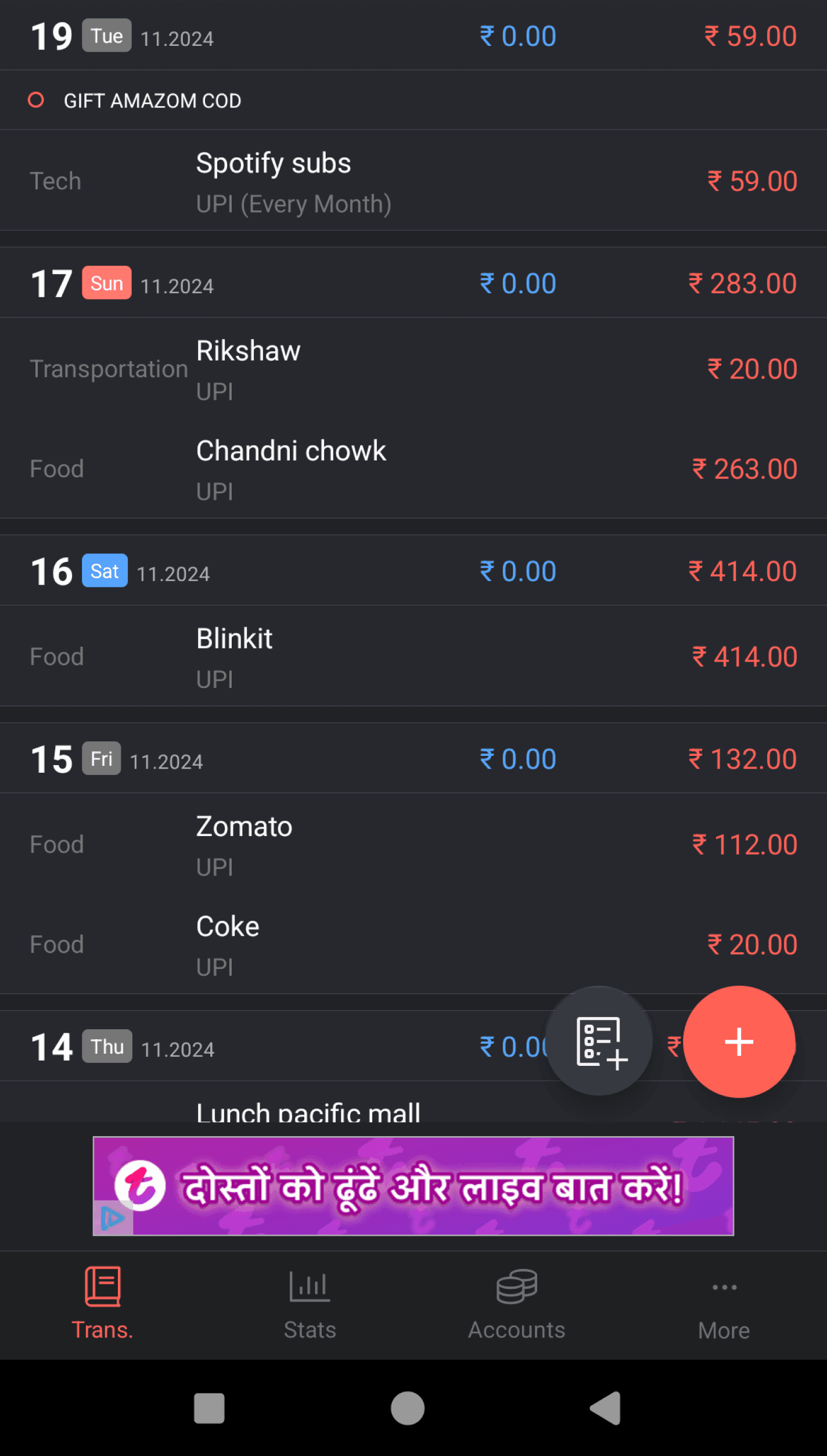

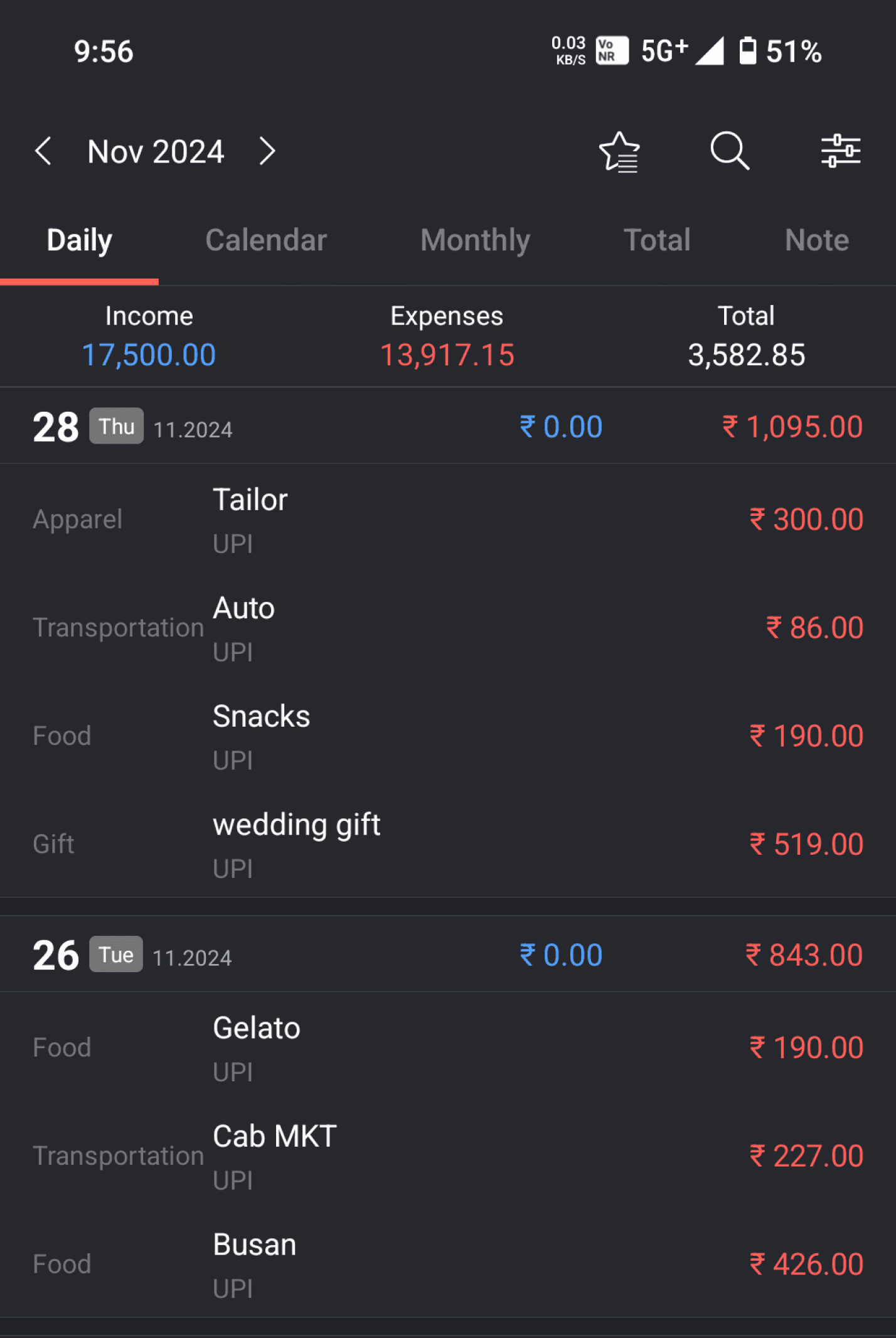

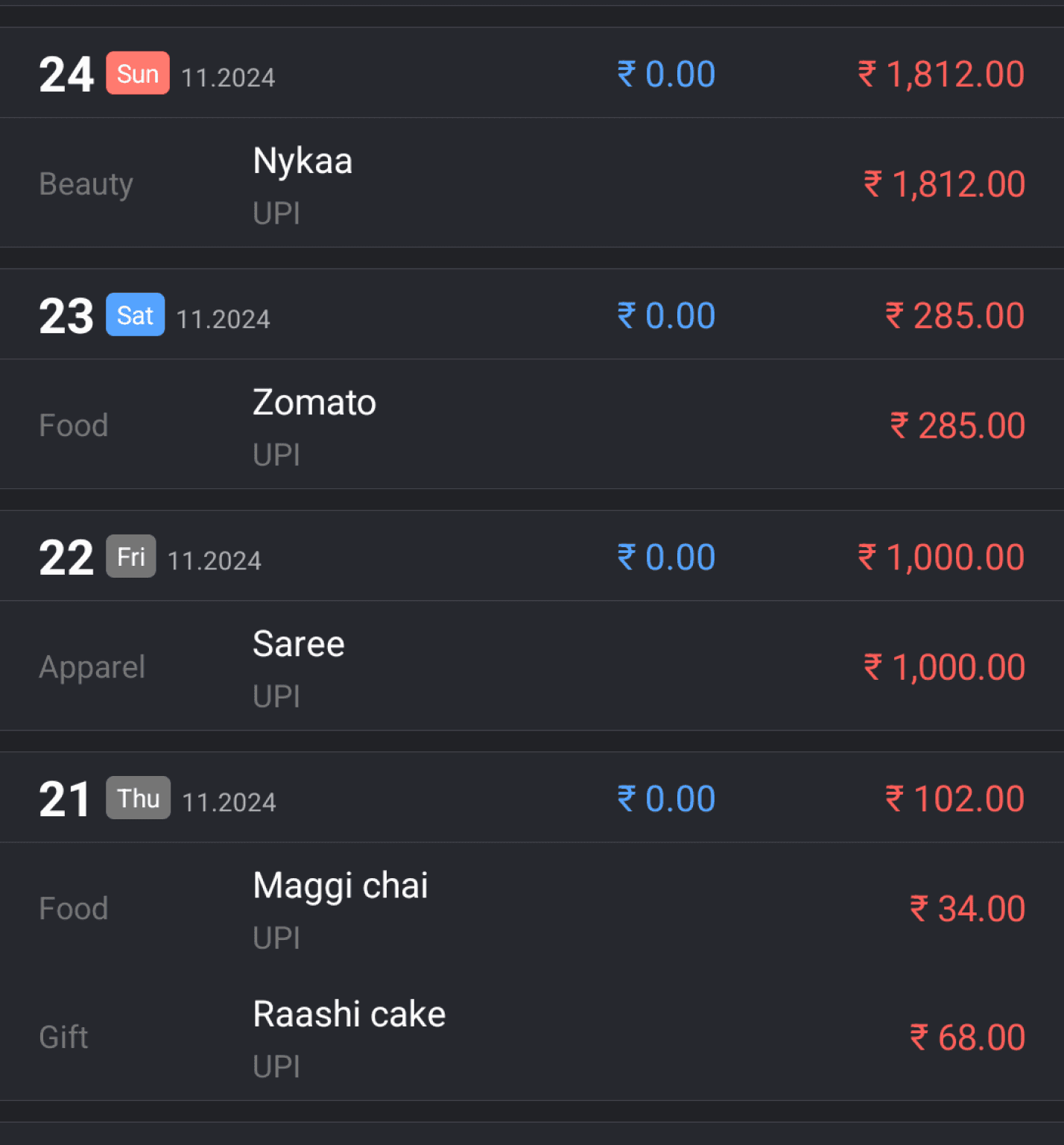

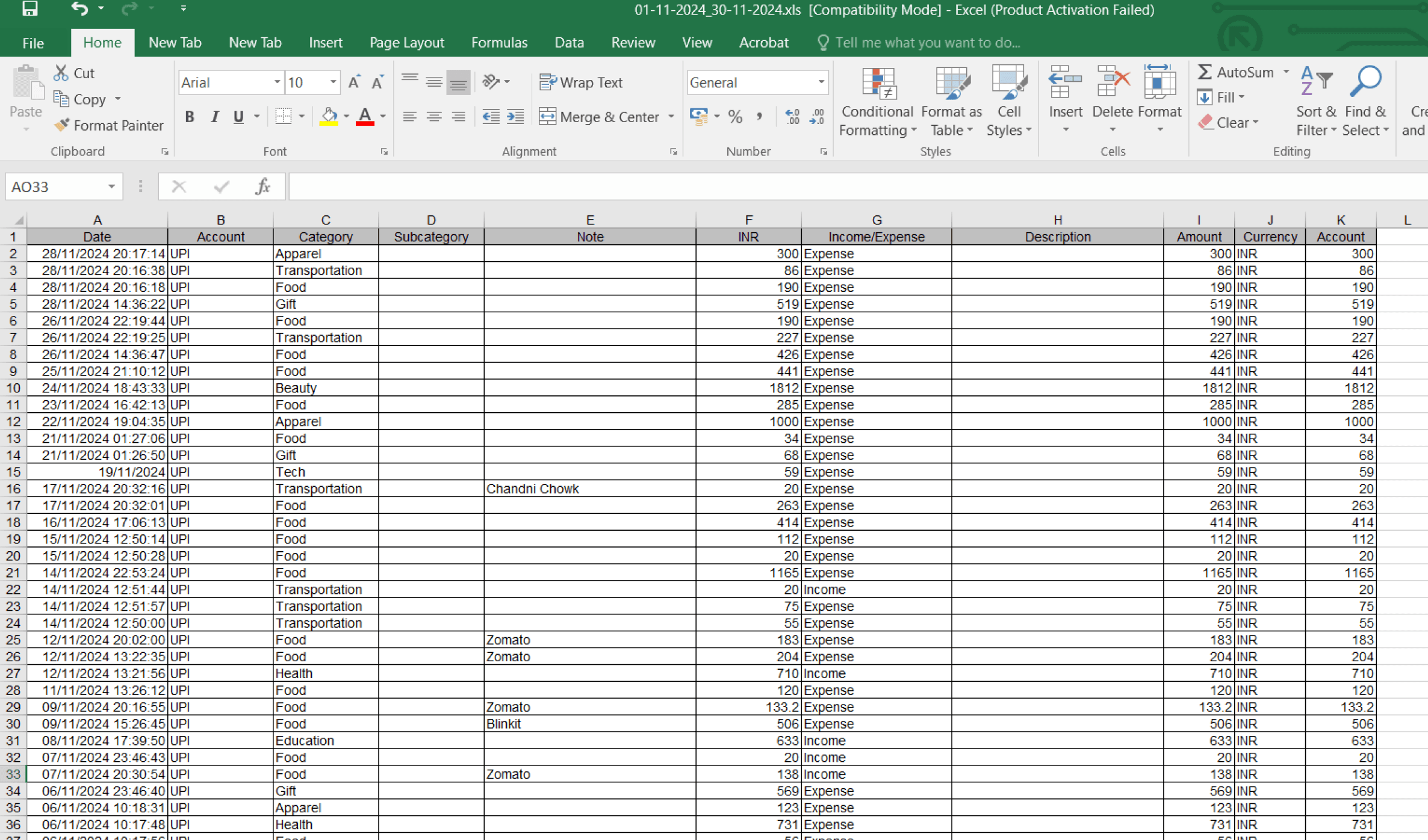

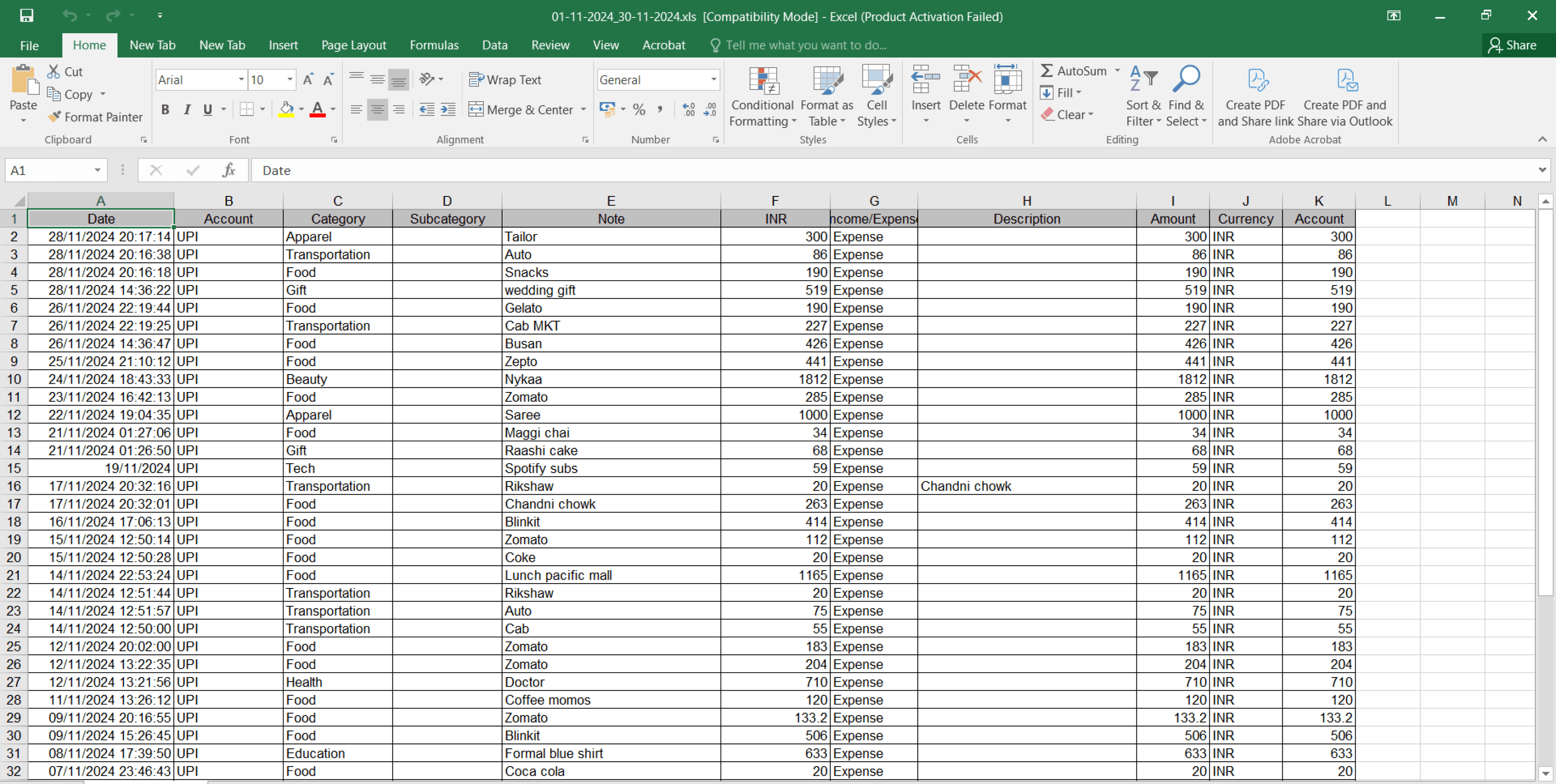

MoneyManager, one of the best personal finance managing app lack automation which when include will make this app more robust and reduce the pain of making each transactions entry manually.

Data Import

Simplify and partially automate the expense tracking system for ease of use

Information Architecture

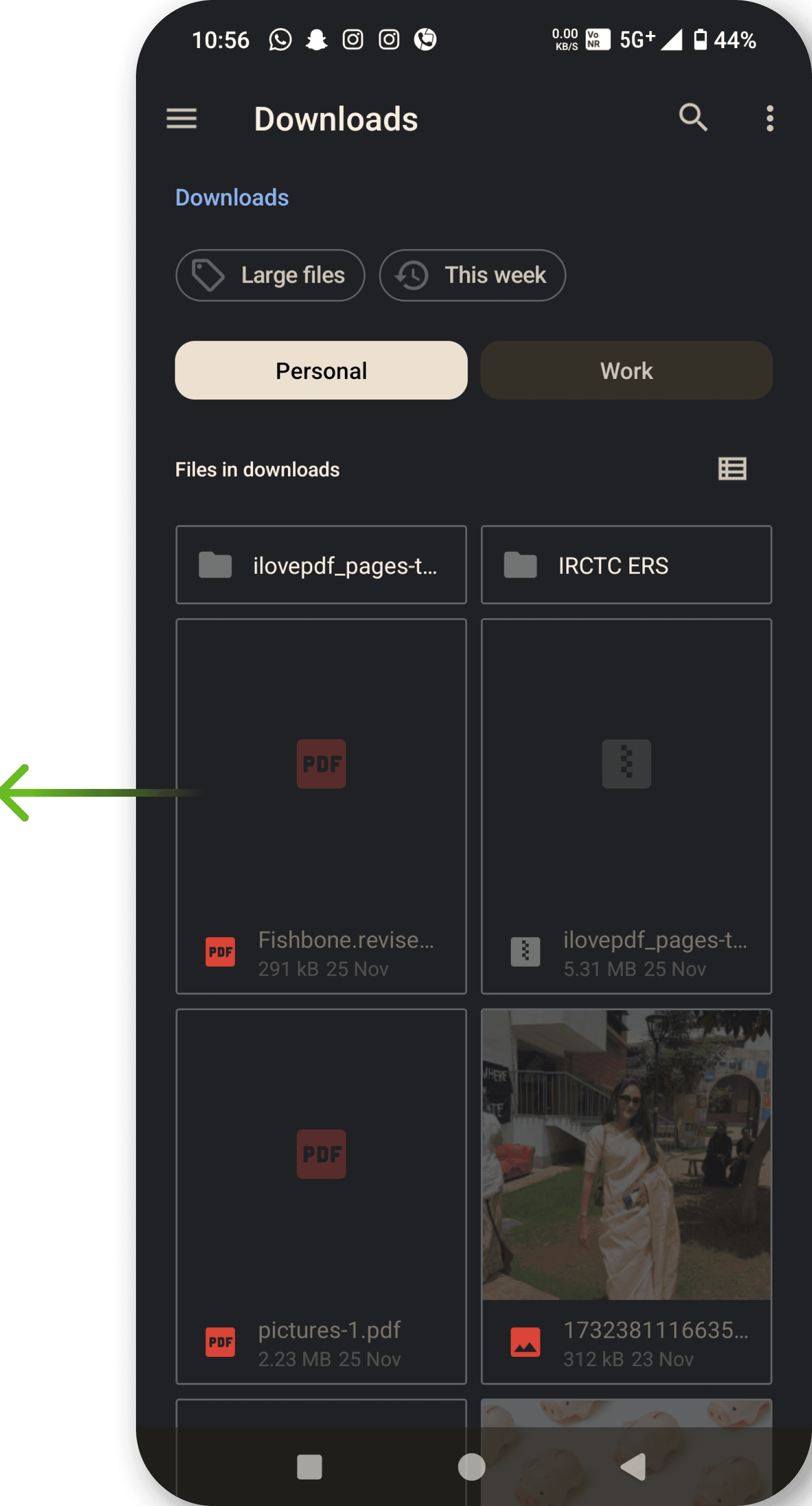

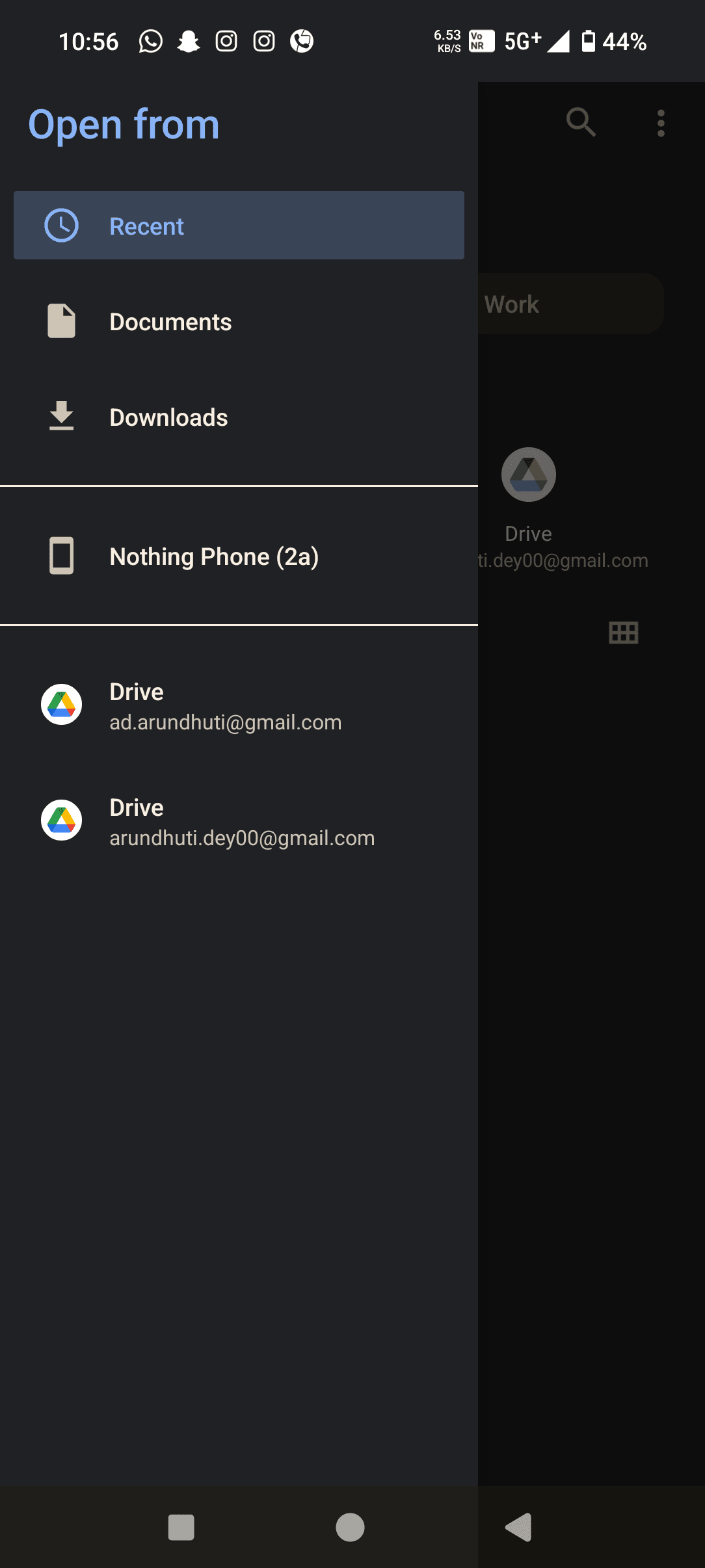

User Flow: Import a .tsv file from device storage

User Flow: Import a .tsv file from device storage

User Flow: Import a .tsv file from device storage

Hit Import Excel File to load the transaction list into the app

increases the convenience level of the user

The app is compatible with .tsv and .xlsx file import formats. This allows for an easy integration with multiple online payment apps.

The only requirement is for other apps to support compatible file export format

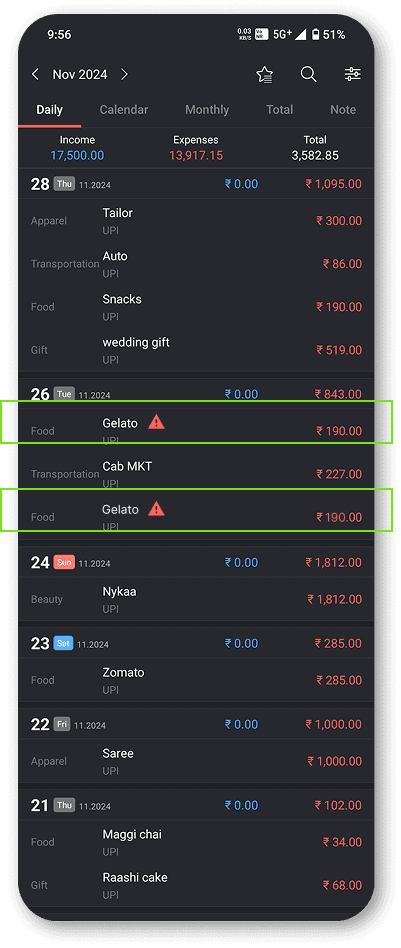

After loading, it allows the user to view it as one complete transaction log which can be viewed and edited as per user need.

The app flags possible overlapping entries to review and solve.

Gelato

190

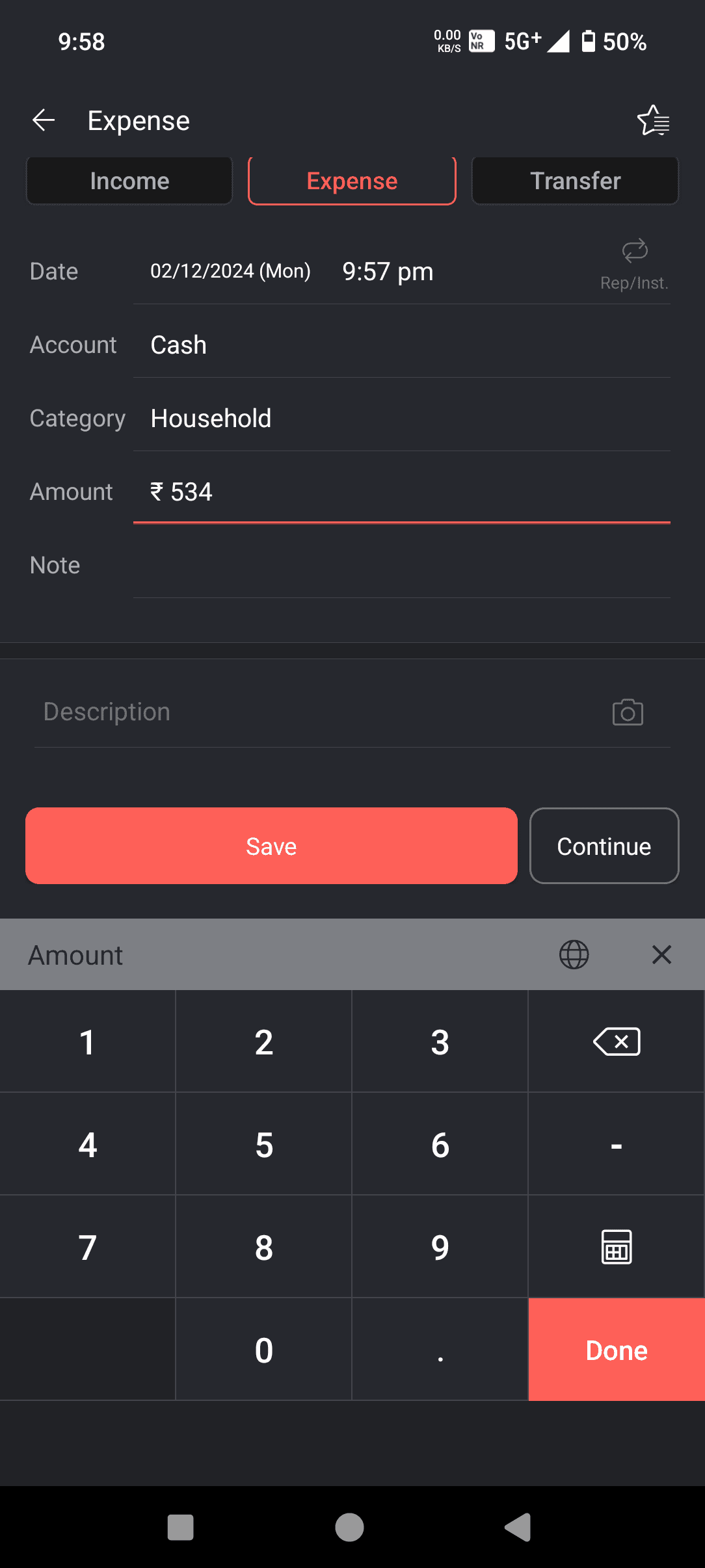

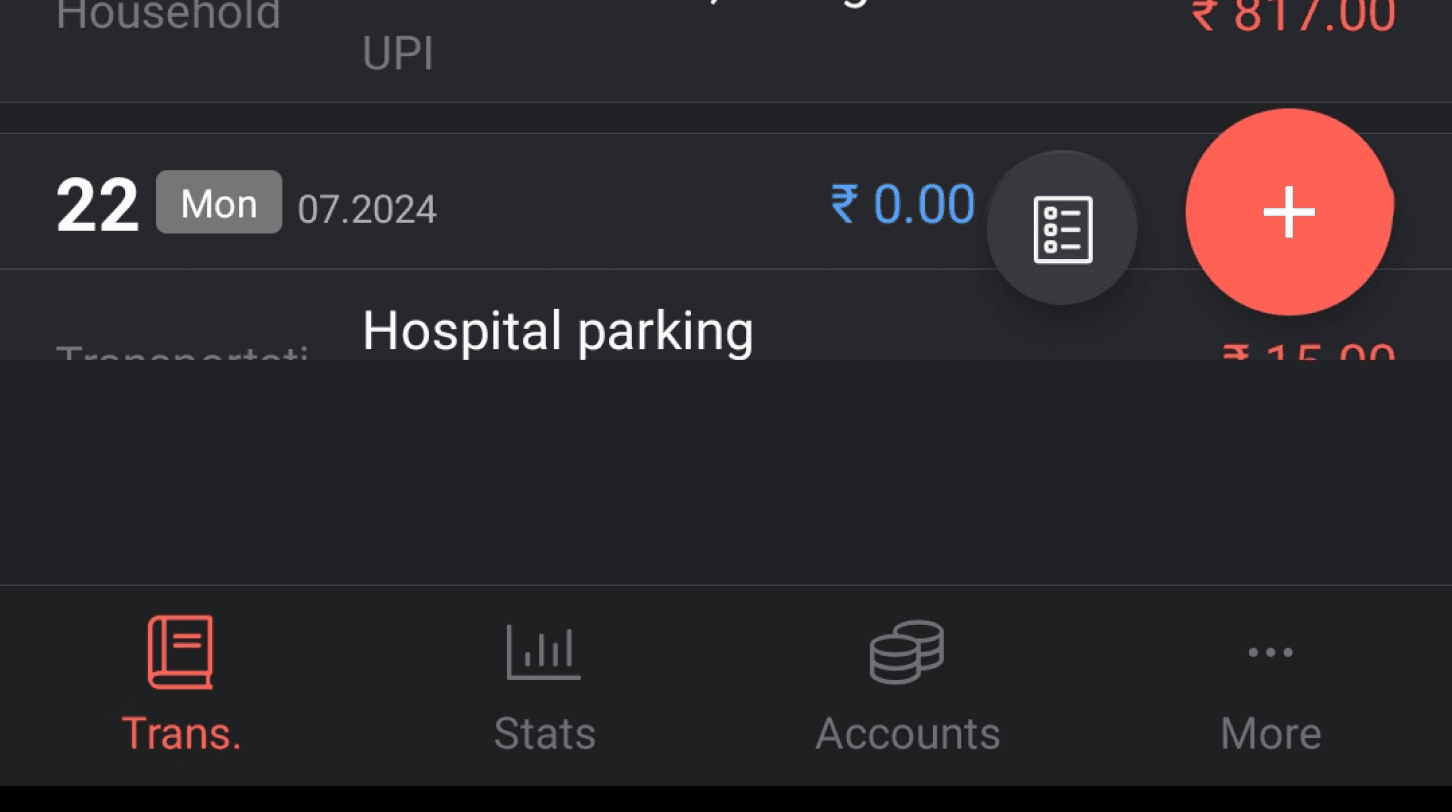

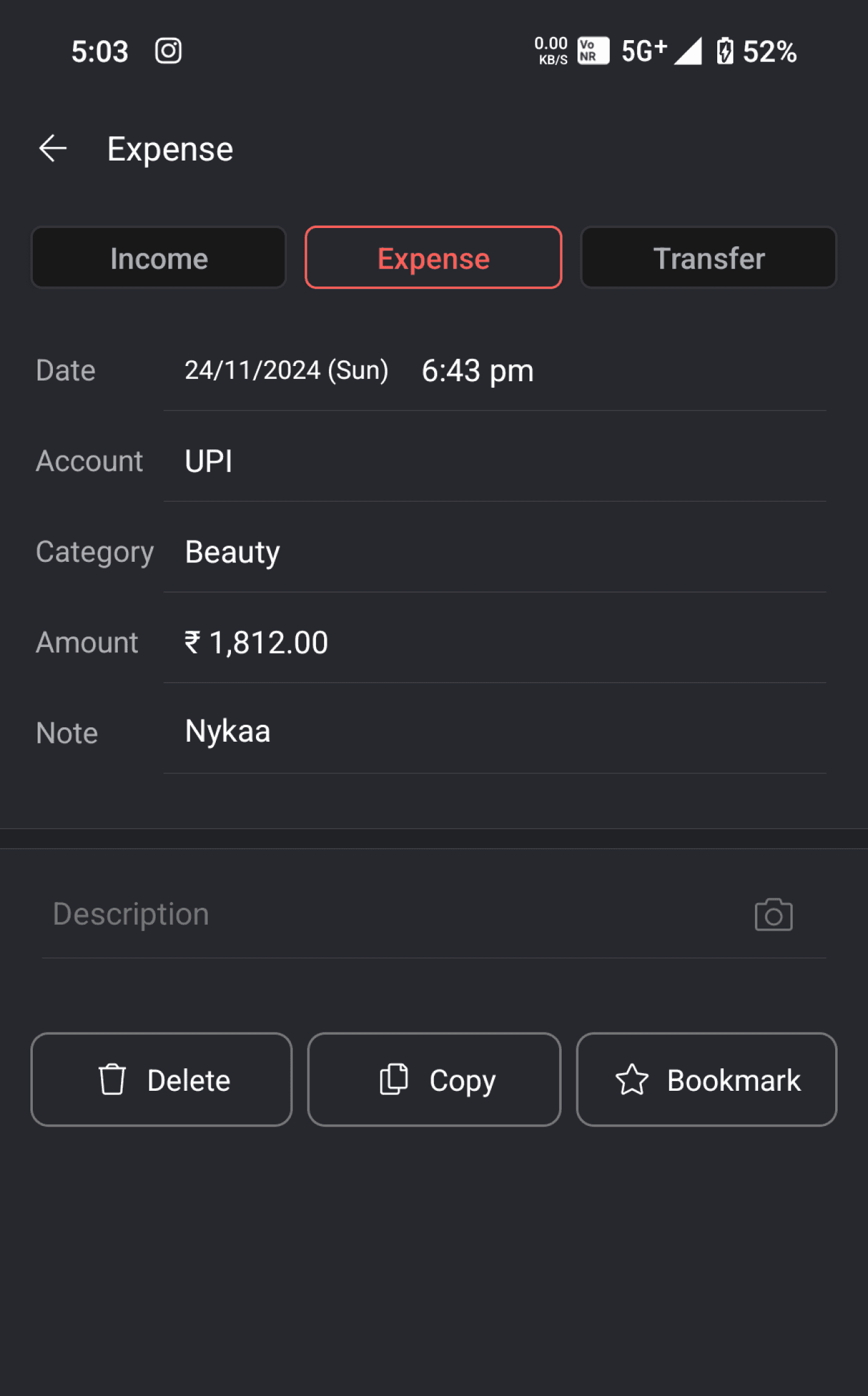

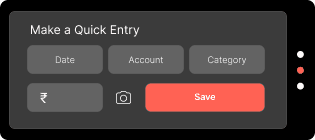

Manual Entries for Cash Transactions

integrate a standardised export format for GPay app.

creates cross-app compatibility which can be later expanded to various apps

Mandatory Categories - Account,

Category

without which import will fail

*Format accepted by Money Manager App - standardised format

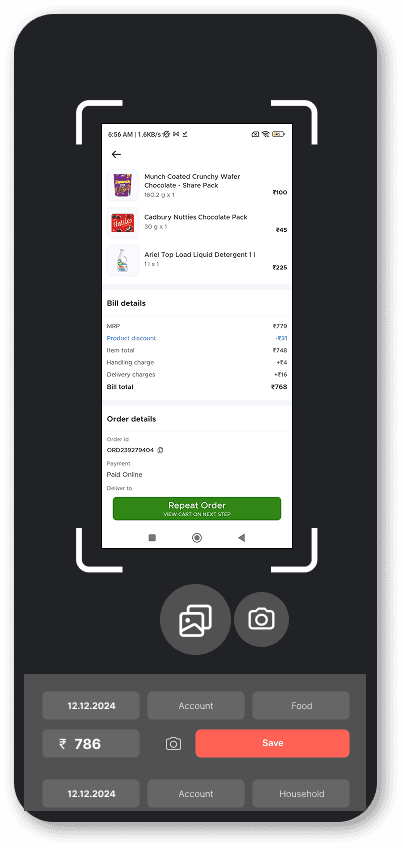

Screenshot Invoice Upload

Introducing an AI feature to read bill screenshots and images, and fill in details; reads texts and fills in details.

Floating Home Screen Widgets & Notifications

Introducing an AI feature to read bill screenshots and images, and fill in details; reads texts and fills in details.

This AI lens feature allows the user to upload a bill image to read transaction details, without the hassle of having to make entries in case a physical or online bill is available.

It reads each item and makes categorisation through AI learning

Click picture on Camera

Take from Gallery

12.12.2024

₹ 786

Account

Save

Food

12.12.2024

Account

Household

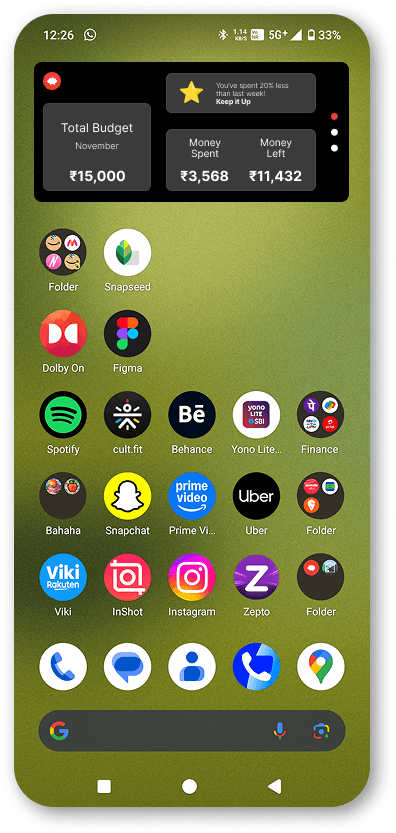

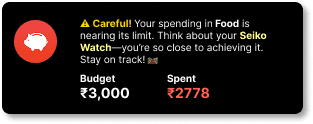

Notification to warn about exceeding limit

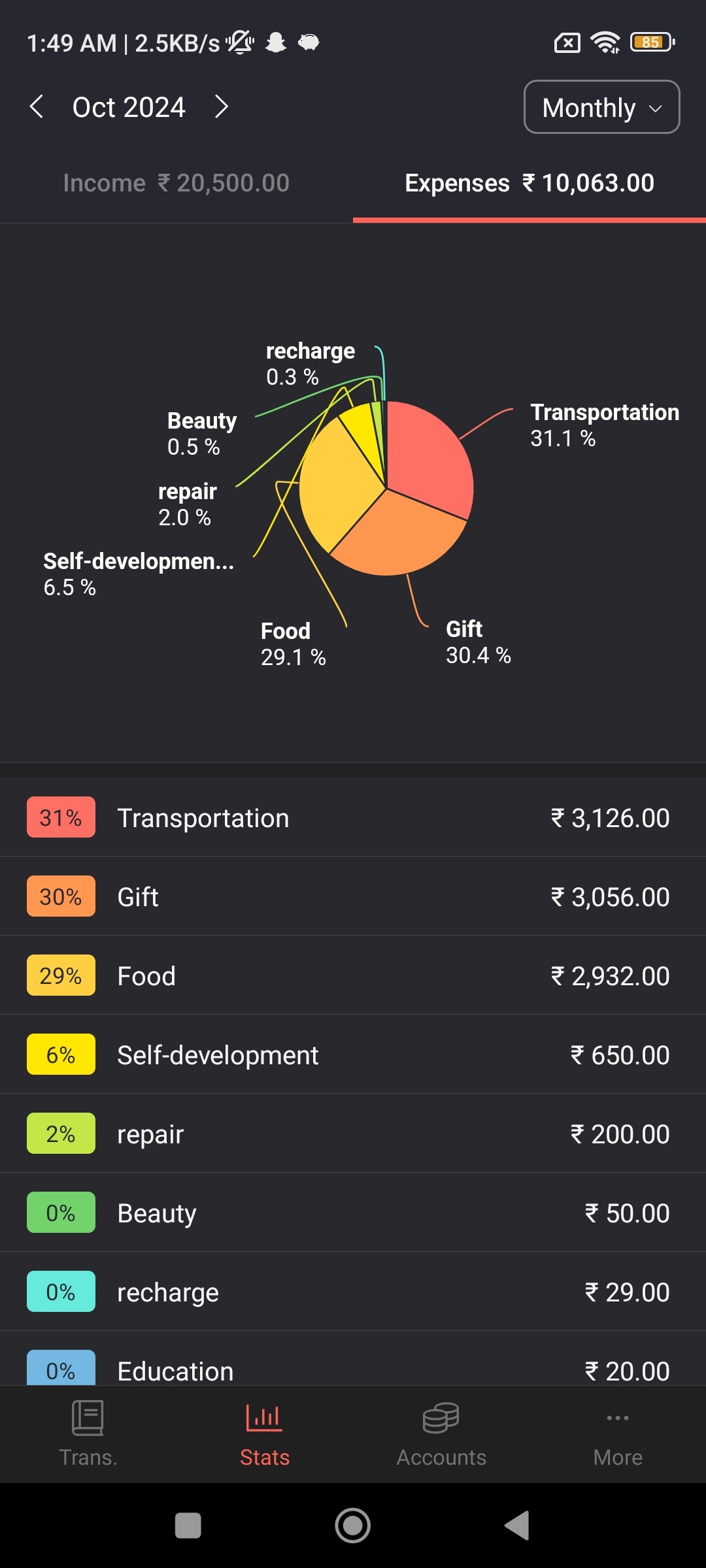

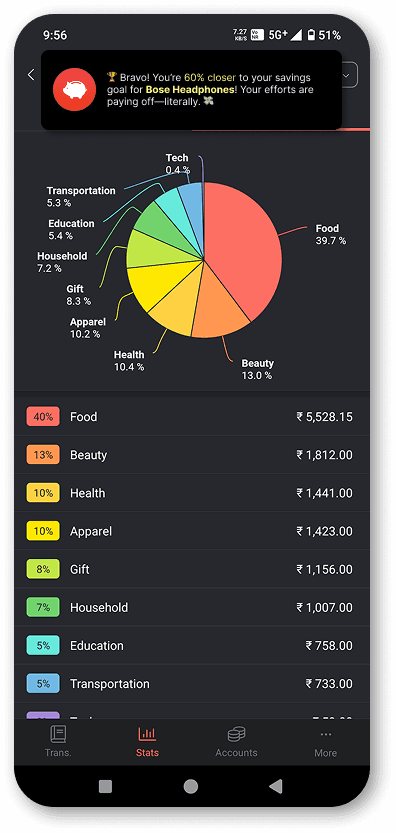

The widgets help with quick summaries to be on top of one’s budget and goals.

🎉 You're crushing it! You’ve stayed within your budget for 12 days! Keep up the great work—you’re getting closer to your financial goals. 💪

⚠️ Careful! Your spending in Food is nearing its limit. Think about your Seiko Watch—you’re so close to achieving it. Stay on track! 🛤️

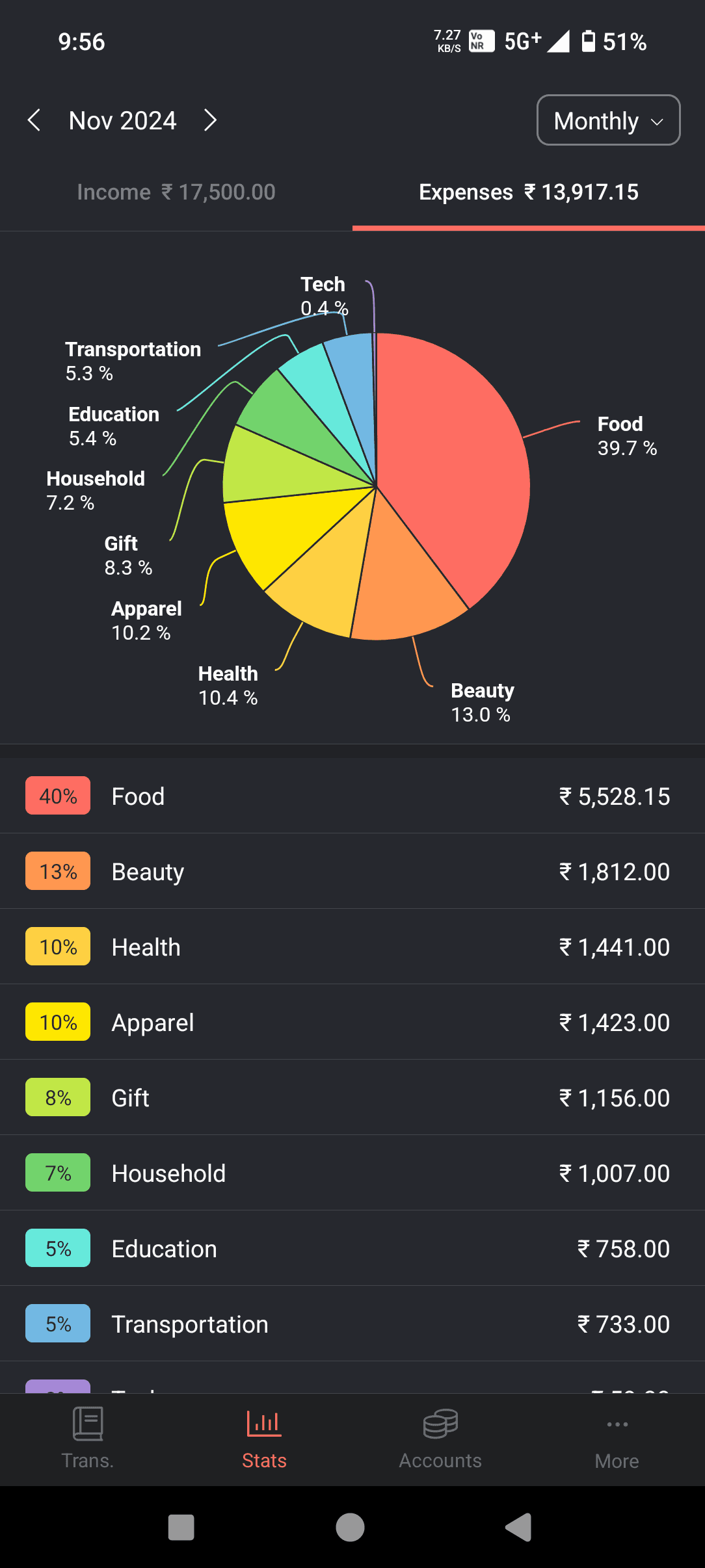

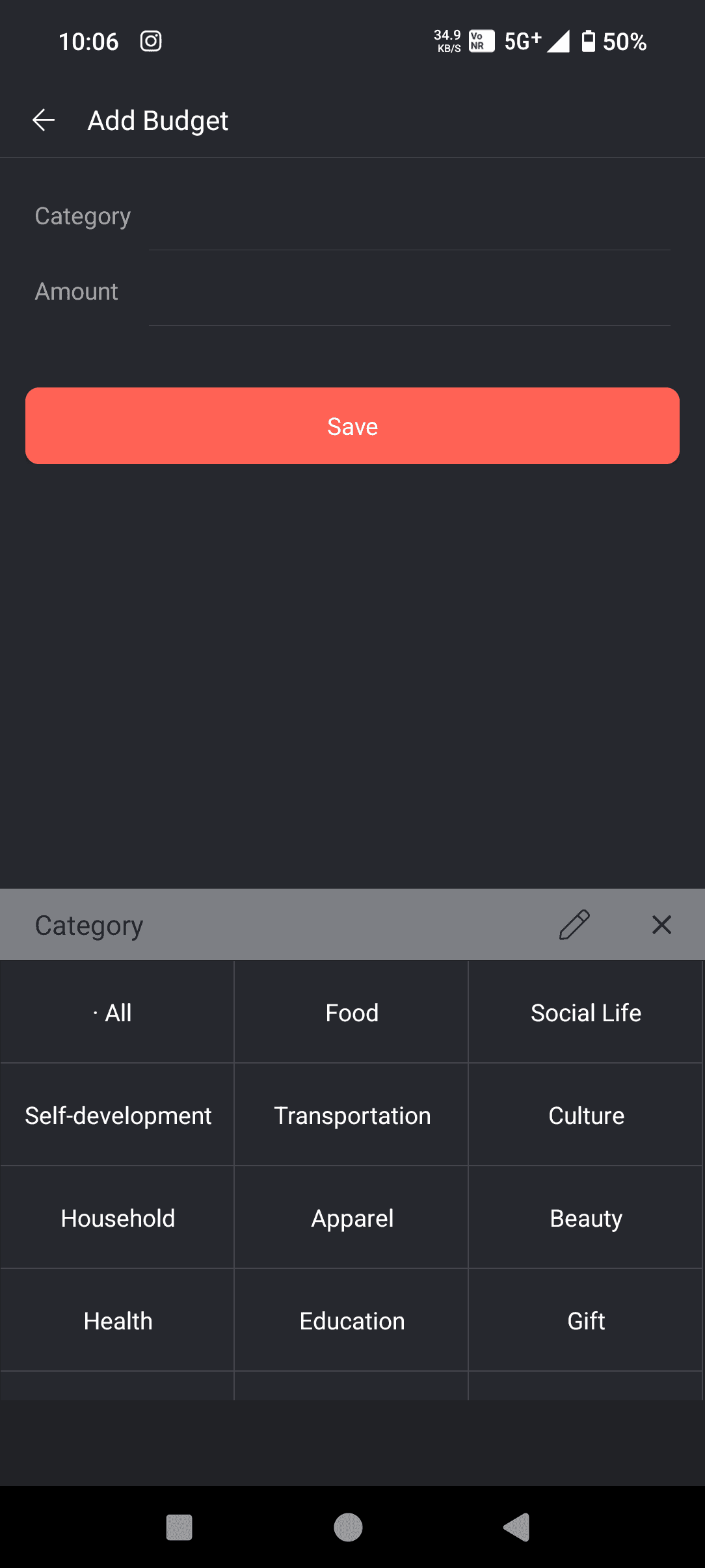

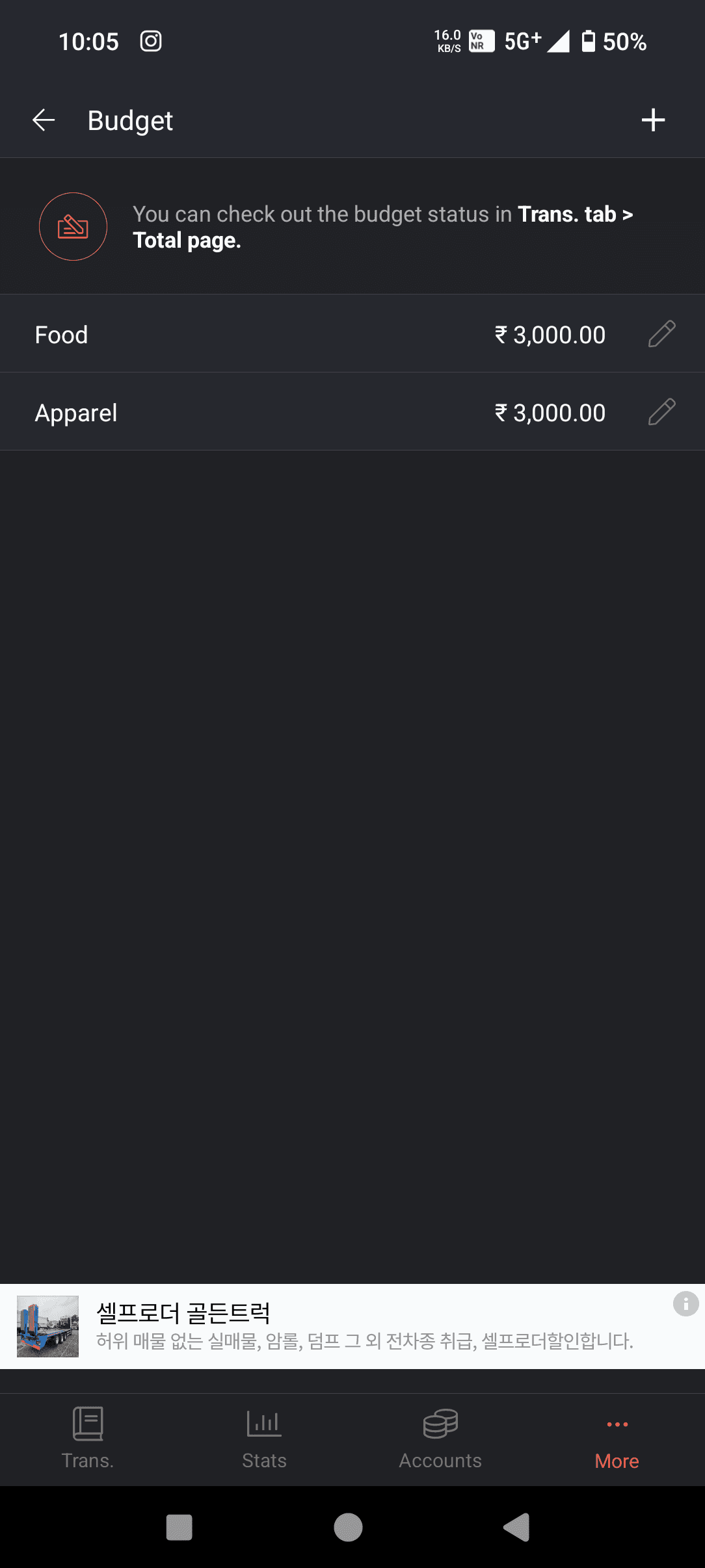

Budget

Spent

₹3,000

₹2778

positive affirmations for goals provides encouragement

🏆 Bravo! You’re 60% closer to your savings goal for Bose Headphones! Your efforts are paying off—literally. 💸

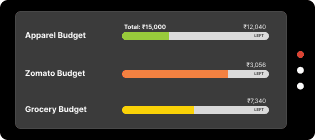

Total Budget

November

₹15,000

Money Spent

₹3,568

Money Left

₹11,432

You’ve spent 20% less than last week!

Keep it Up

Apparel Budget

₹12,040

LEFT

Total: ₹15,000

Grocery Budget

₹7,340

LEFT

Zomato Budget

₹3,056

LEFT

Make a Quick Entry

Date

₹

Account

Save

Category

This application permits widget display, providing concise insights at a single look

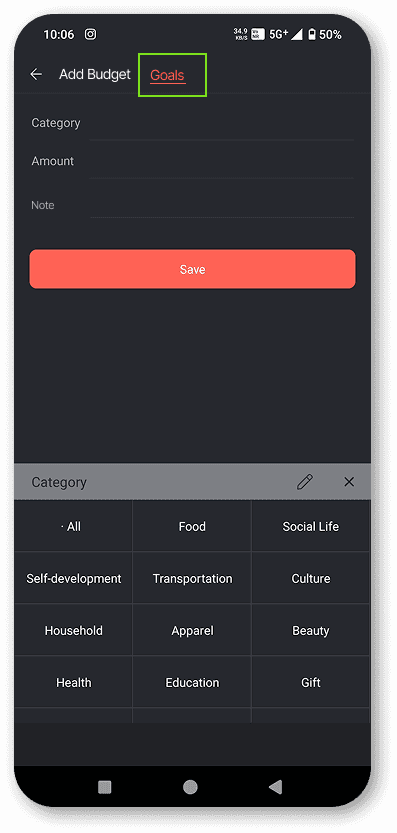

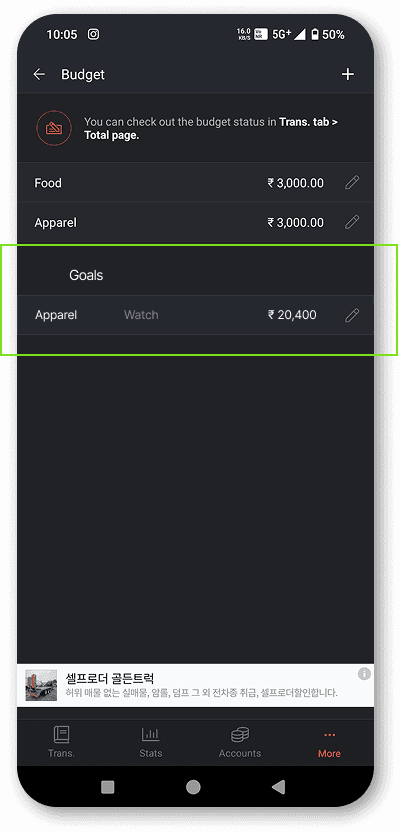

Goals

Note

Add Budget

Adding personal goals for motivation

Goals

Apparel

Watch

₹ 20,400

Mark as Refunded

Manually recording a refund brings that comfort of getting back money

02

Freemium App

MoneyManager App Integration

MoneyManager, one of the best personal finance managing app lack automation which when include will make this app more robust and reduce the pain of making each transactions entry manually.

Data Import

Simplify and partially automate the expense tracking system for ease of use

Information Architecture

User Flow: Import a .tsv file from device storage

The app is compatible with .tsv and .xlsx file import formats. This allows for an easy integration with multiple online payment apps.

The only requirement is for other apps to support compatible file export format

increases the convenience level of the user

*Format accepted by Money Manager App - standardised format

Mandatory Categories - Account,

Category

without which import will fail

integrate a standardised export format for GPay app.

creates cross-app compatibility which can be later expanded to various apps

After loading, it allows the user to view it as one complete transaction log which can be viewed and edited as per user need.

The app flags possible overlapping entries to review and solve.

Manual Entries for Cash Transactions

Mark as Refunded

Manually recording a refund brings that comfort of getting back money

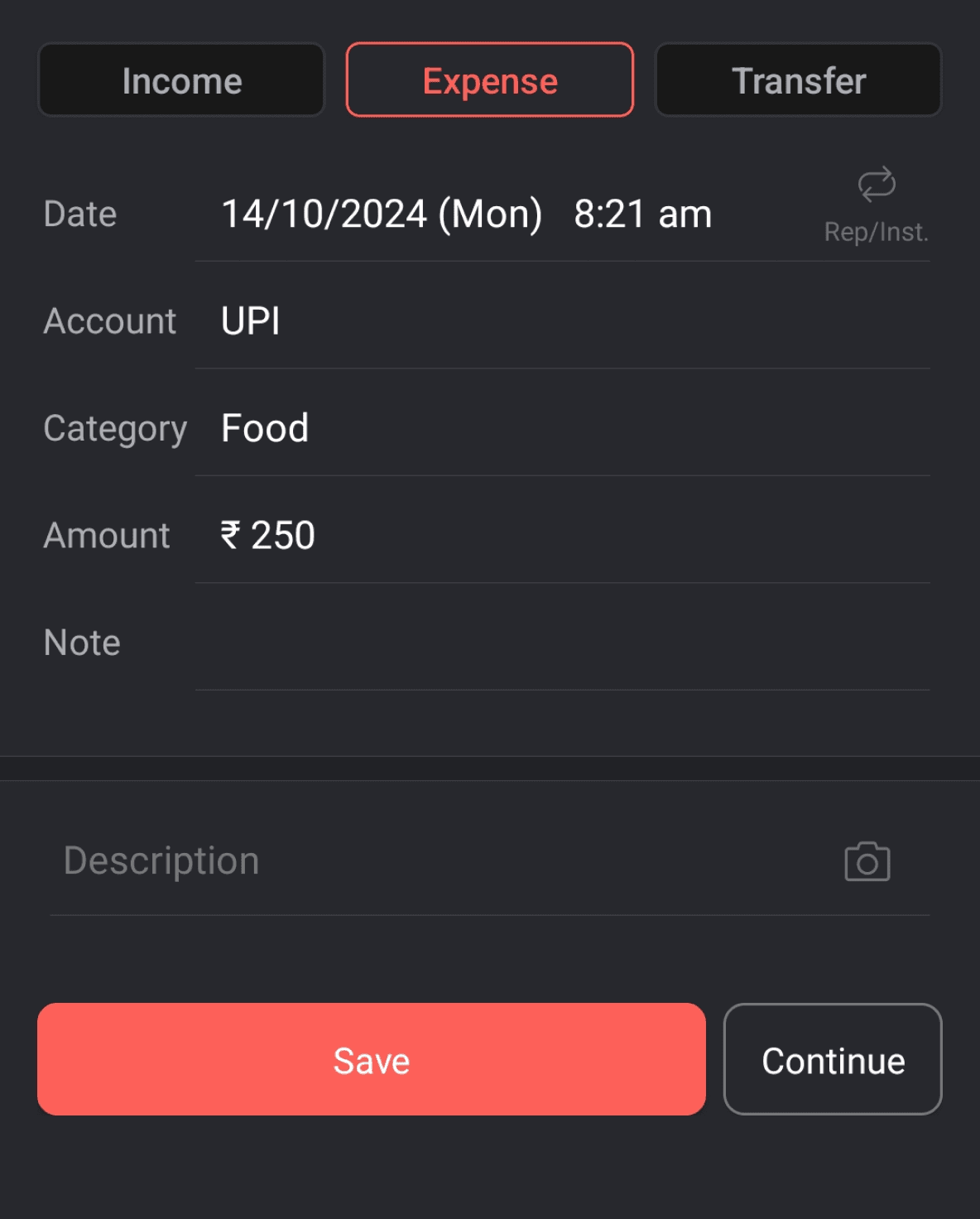

User Flow: Add an expense entry with a bill image

Screenshot Invoice Upload

Introducing an AI feature to read bill screenshots and images, and fill in details; reads texts and fills in details.

Take from Gallery/ Click picuture

This AI lens feature allows the user to upload a bill image to read transaction details, without the hassle of having to make entries in case a physical or online bill is available.

It reads each item and makes categorisation through AI learning

Floating Home Screen Widgets & Notifications

Introducing an AI feature to read bill screenshots and images, and fill in details; reads texts and fills in details.

This application permits widget display, providing concise insights at a single look

Notification to warn about exceeding limit

The widgets help with quick summaries to be on top of one’s budget and goals.

Adding personal goals for motivation

positive affirmations for goals provides encouragement

User Flow: Import a .tsv file from device storage